INFLATION BREAKEVENS: STILL A CORE HOLDING

The 'tourist talks about his favourite investment

MESSAGE FROM THE MACROTOURIST: You’re receiving this email because you signed up for the free version of my newsletter. About four years ago, I switched to a paid product, and promised I would never fill your inbox with promotions or other attempts to get you to sign up. Staying true to that commitment, I am sending the full piece that I sent out to my paid subscribers a month ago. I’m sharing it with you because I am passionate about inflation breakevens—their time has come—and I am looking for others who feel similarly. If that’s you, contact me. Otherwise, thank you for your time, and rest assured my pledge stands. You will never receive half-exposed articles designed to entice you to subscribe; it’s either a full MacroTourist piece or nothing.

INFLATION BREAKEVENS: STILL A CORE HOLDING

the ‘Tourist talks about his favourite investment

originally sent to subscribers on December 3rd, 2024

Over the past few years, we’ve all been reminded that inflation is not something confined to the dustbin of history. We feel the rising prices at the grocery store or when buying lunch at the office. But inflation doesn’t just affect the things that we buy. It changes the entire way we need to look at our investments.

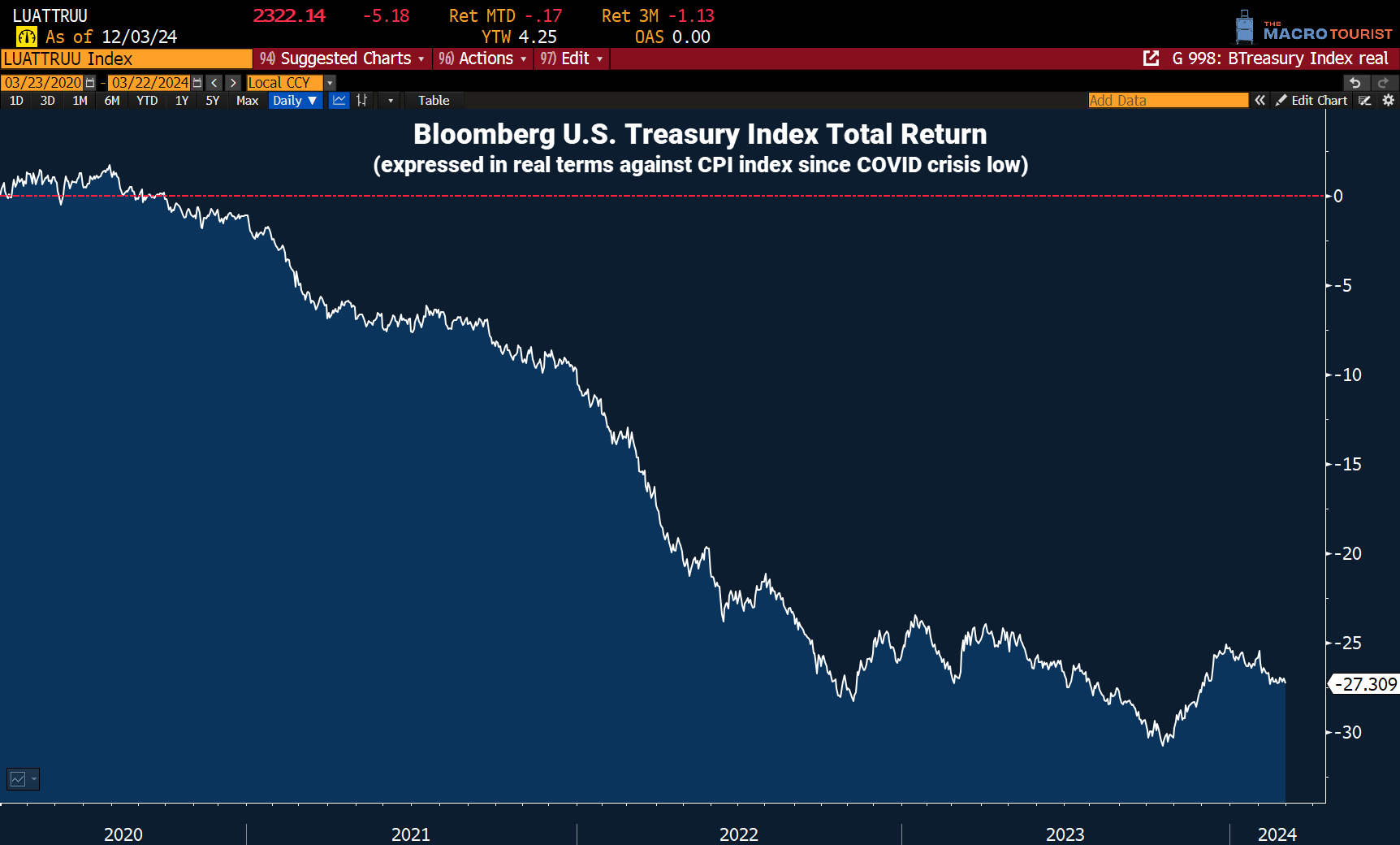

If you simply left your money in cash and earned the interest rate set by the Federal Reserve, then, since the start of 2020, you will have whittled your purchasing power of one dollar down to $0.914 in real terms. You might say that’s not a fair comparison, often investors earn a higher yield by buying longer-dated bonds. For many years, investing in longer-dated Treasury securities appeared to offset some of the insidious erosion caused by inflation, but in the wake of the COVID-crisis, bond investors fared even worse. Since the March 2020 COVID-crisis low, the Bloomberg U.S. Treasury Index lost 27.3% in CPI-adjusted-real-terms.

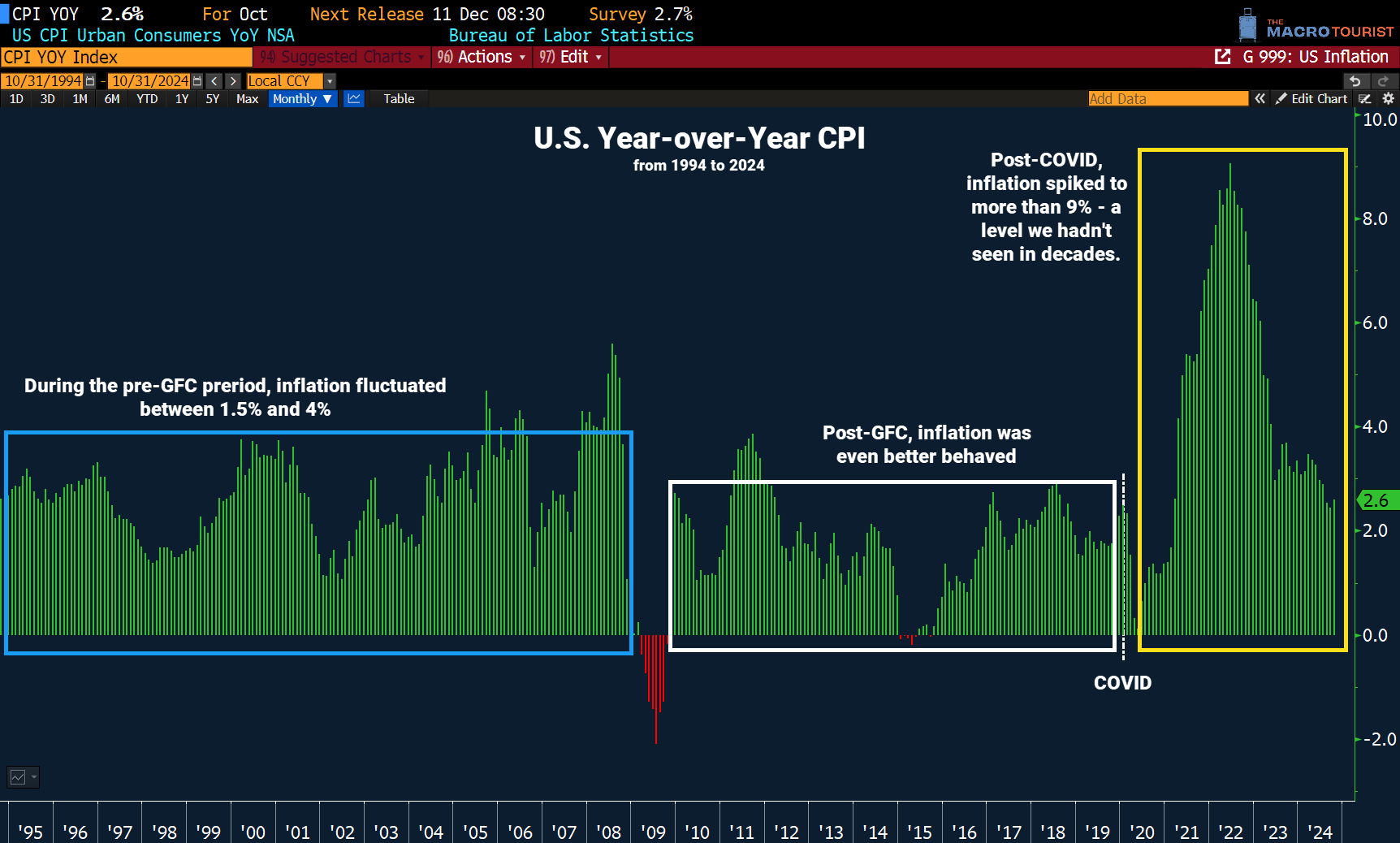

This poor performance can be explained by the fact that, since COVID, inflation has become a bigger problem than any other time in the past three decades.

This inflationary spike has since cooled down, and many market participants believe the inflationary period from 2021 to 2023 was an aberration. These investors are content to allocate to traditional bond products on the assumption that interest rates and inflation will soon return to pre-COVID levels.

On the first draft of this piece, I wrote an entire section explaining the reasons that I believe inflation will continue to be a persistent problem. However, I removed it. I didn’t want to muddy the message. Let’s face it, determining the path of future inflation is extremely difficult. Having another debate about the potential problems our economy faces is not where I can add the most value.

Instead, I’d rather talk about an investment strategy that can mitigate inflation risk — inflation breakevens.

Portfolios need an inflation solution

As we move from a disinflationary to inflationary environment, investors need to add a new tool to their portfolios. Inflation breakevens are an essential strategy for navigating this new reality.

If inflation breakevens are so great, why haven’t they become more popular already?

In a low inflation environment such as the previous decade, there was little demand as most investors were more worried about deflation. Although it now seems obvious that inflation was lurking below the surface, only five years ago, the Federal Reserve was openly worried about being able to create enough inflation.

But what are inflation breakevens? Are they simply buying TREASURY INFLATION PROTECTED SECURITIES (also known as TIPS)?

No, inflation breakevens are different.

Although buying TIPS is part of the inflation breakeven strategy, the problem with TIPS is that they are still bonds. The interest TIPS pay is partly based on inflation, but TIPS still move up and down with interest rates. A TIPS holder is not solely investing in inflation, but a combination of a government bond with an inflation component.

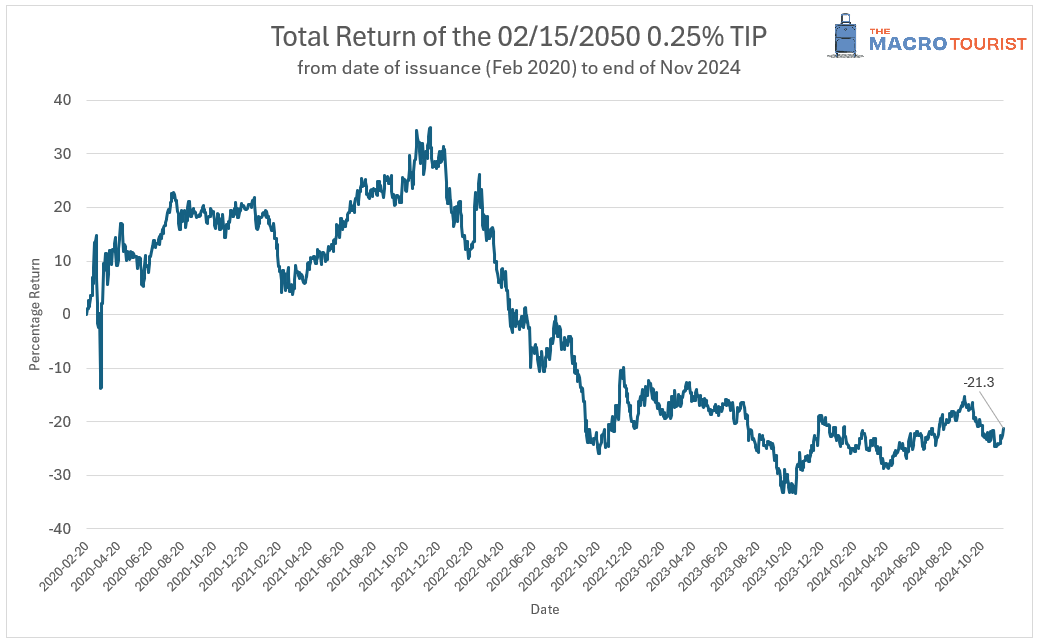

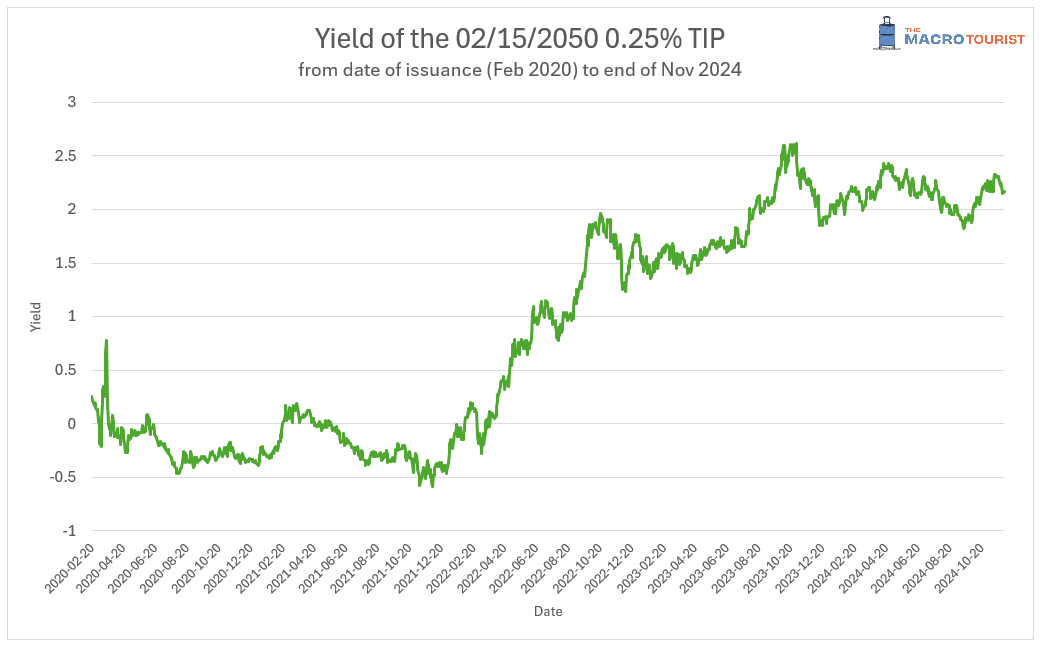

Let’s look at a specific example to better understand the problem with TIPS. During the COVID crisis, if you decided that inflation would increase, you could have bought the 30-year TIP that matures February 15th, 2050. The yield on that TIP was minus 50 basis points. That meant that over the next thirty years, an investor would receive the CPI rate minus 50 basis points.

In 2021, inflation ended the year at 7%. In 2022, inflation spiked to 8.5% and finished at 6.5%. An investor that owned TIPS over this period received those inflation rates as interest payments. Those were some hefty coupon payments.

The investor in that 30-year TIPS bond issue must have been ecstatic, right?

Although the inflation payments were sizeable, during this period, interest rates also rose. Putting together the interest payments along with the change in the TIP’s value, the total return for this TIPS issue ended up being negative. It actually lost 21.3% (in nominal terms) from issuance to today. Given that we just went through one of the largest bouts of inflation in decades, this is a disappointing performance.

It’s a common complaint about TIPS; in periods of inflation, the rise in interest rates hurts the bond portion of the security. During other periods, the lack of inflation drags down the current yield versus the traditional nominal bond.

To better understand what happened, here is the graph of our 30-year TIPS yield. It started at minus 50 basis points, but rose 250 basis points to positive 2%.

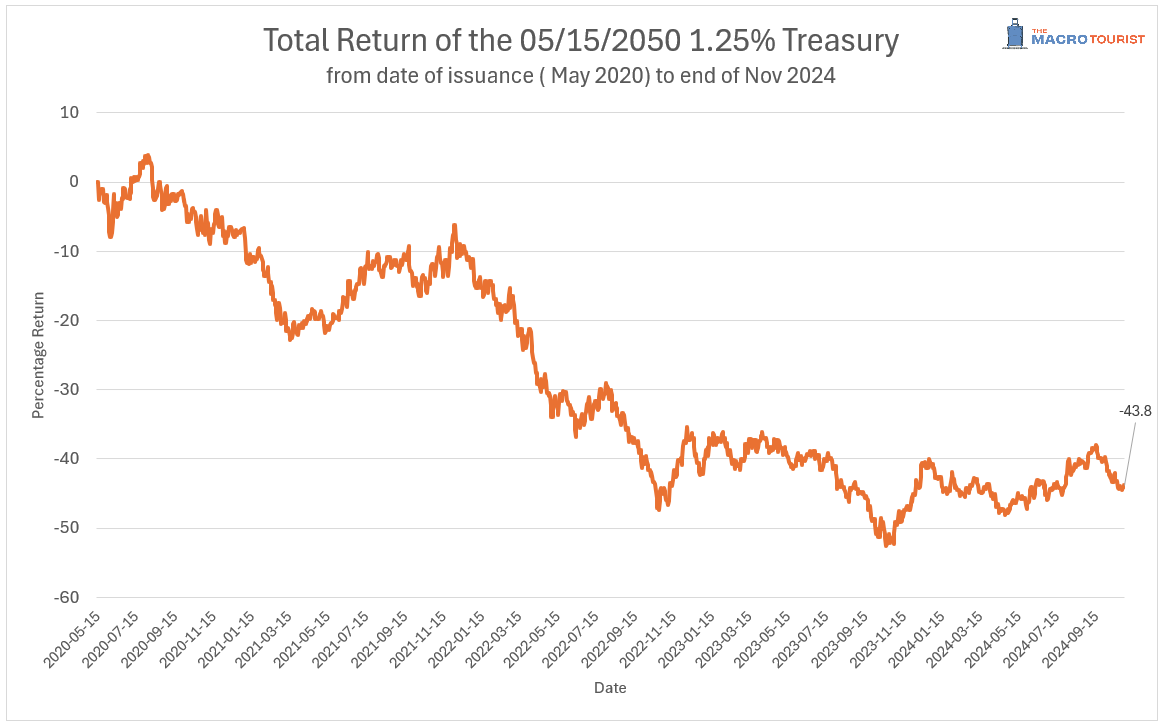

Although TIPS might not be the ideal hedge against rising inflation, they perform substantially better than nominal bonds. For example, here is the traditional 30-year bond over the same period.

The 30-year TIP lost 21.3% during this period, but the traditional bond lost almost 44%!

Seeing the return of the TIP and the Treasury bond back-to-back, it’s easier to understand the problem with TIPS. It was the bond portion of the TIPS that dragged down returns, so what is needed is a strategy that isolates the CPI portion of the TIP.

And that’s what inflation breakevens do.

Inflation breakevens in action

To get long inflation breakevens, an investor could have bought the 30-yr TIP and sold short an appropriate amount of 30-year nominal bonds, leaving them solely exposed to future CPI levels. If over the life of the bond, inflation ended up being higher than the “inflation breakeven” level, the investor would benefit.

There is no doubt that this is not an easy strategy to implement. An investor needs to duration match the different securities and then maintain the proper hedge ratio over the life of the bonds.

It might take some extra work, but it’s worth it. In this era of secularly higher inflation, inflation breakevens are a crucial building block for portfolio construction.

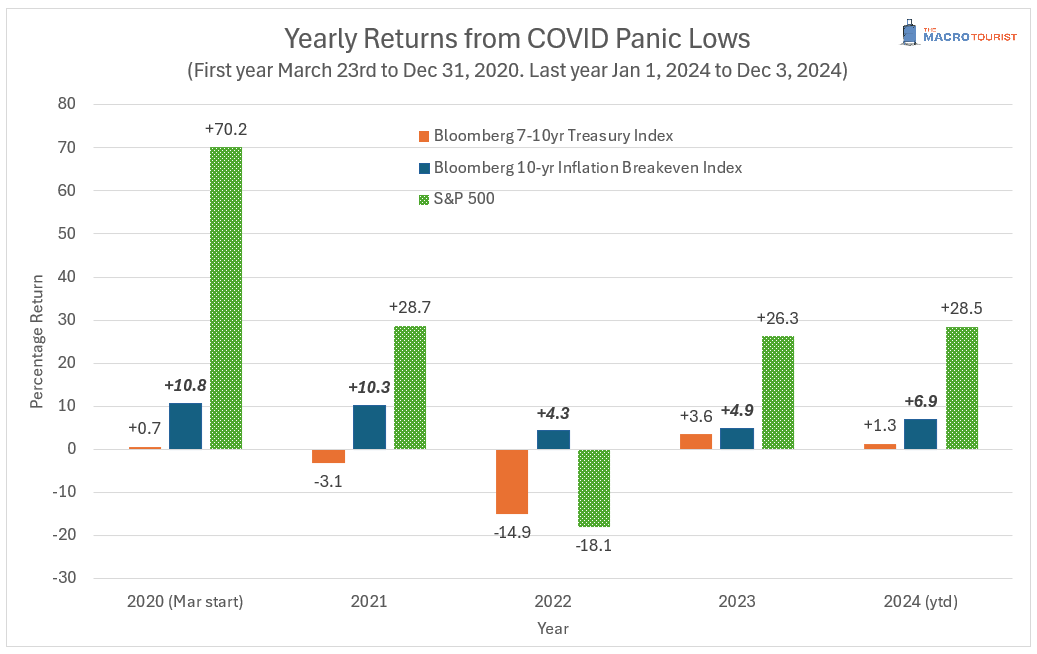

In 2022, the traditional 60/40 portfolio (60% equity and 40% bonds) experienced the worst performance in decades. The S&P 500 was down 18.1% and the Bloomberg 7-10yr Treasury Index lost 14.9%. Usually, when stocks decline, bonds act as a buffer and stabilize the portfolio. In this case, bonds declined because of the higher than expected inflation and, unfortunately, stocks followed bonds lower.

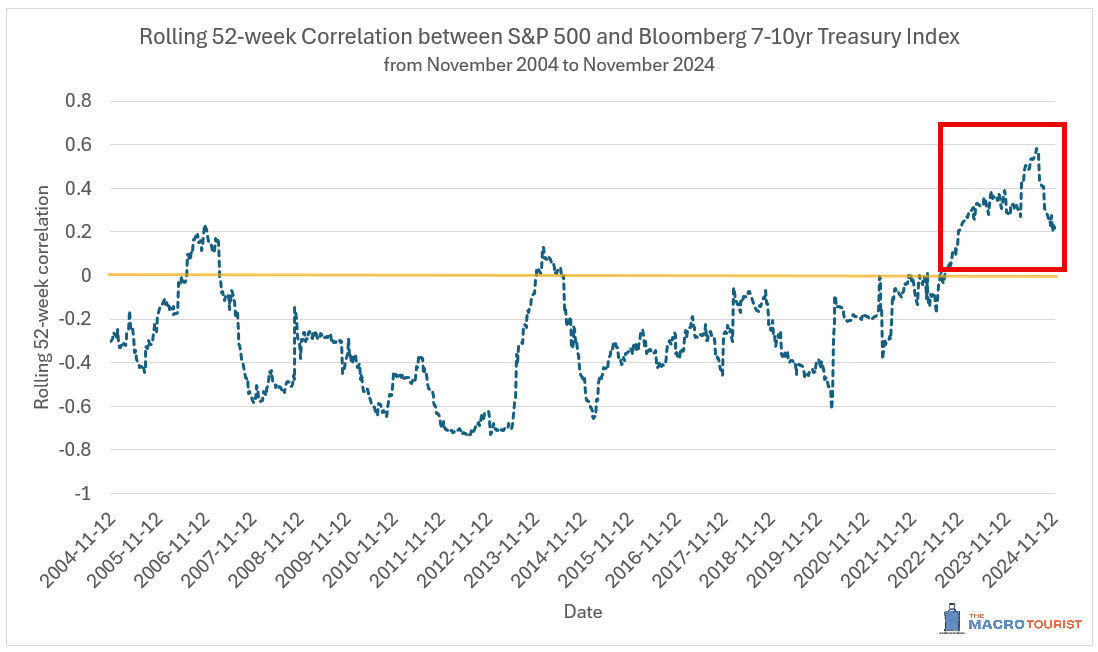

Prior to COVID, stocks and traditional bonds were often negatively correlated. This meant that when stocks fell, investors enjoyed the benefit of positive performance from their bond portfolio.

However, that relationship changed. Stocks and traditional bonds are now positively correlated. Investors need an investment strategy that benefits from higher inflation.

Inflation breakevens are the perfect complement to a stock portfolio in this environment.

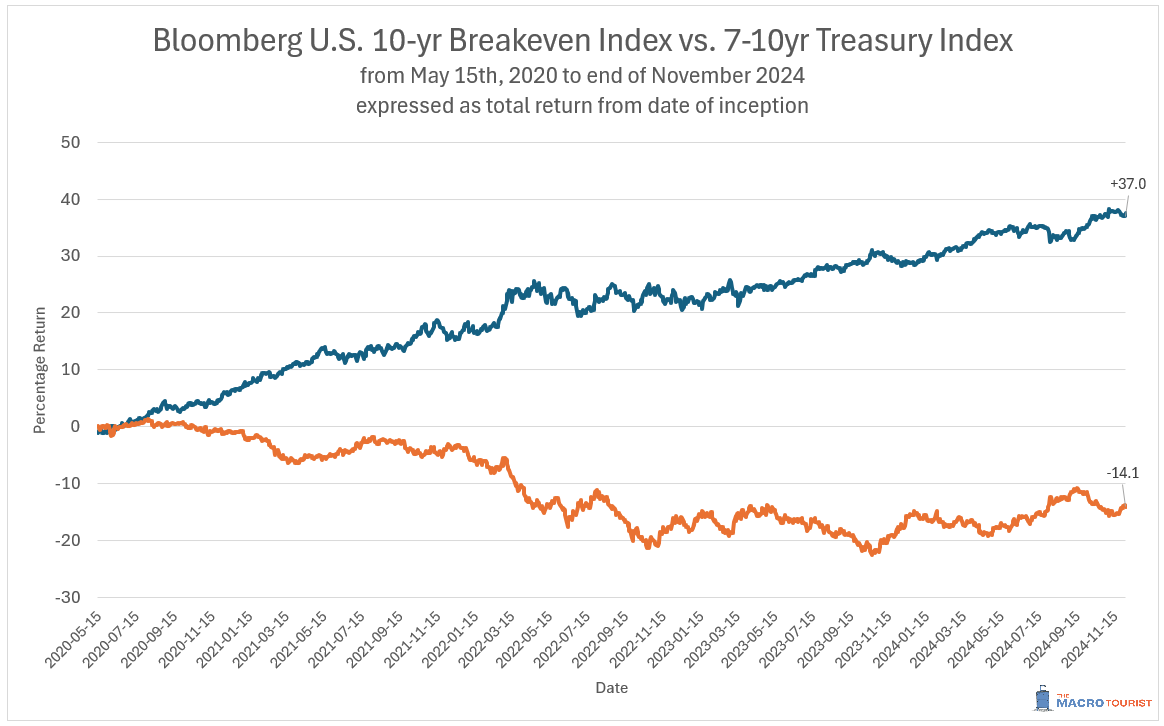

The Bloomberg US 7-10-yr Total Return treasury index returned minus 14.1% during the post-COVID period, while the Bloomberg 10-year Inflation Breakevens index climbed 37.0%.

We have entered a period of secularly higher-than-expected inflation and investors cannot count on traditional bonds cushioning their portfolios. In fact, bonds were expected to be a ballast in a storm, but they could end up capsizing the vessel in an inflationary tempest.

Inflation breakevens are one of the few ways an investor can directly hedge this risk. They are the cleanest and most efficient way for investors to gain direct exposure to an asset that represents future CPI.

Over the years, I have written about inflation breakevens, each time expressing my overenthusiastic love for this strategy.

Although I have written about inflation breakevens extensively, I understand they are difficult for many non-fixed-income specialists to trade. In the coming weeks, I will detail how individual traders can go about replicating this strategy.

In the meantime, I believe in this strategy so much; I am working on creating an ETF to allow investors easy access to what should be a cornerstone portfolio construction tool. In the future, inflation breakevens will not be a specialty strategy practiced only by sophisticated pension funds and endowments, but an essential portfolio complement for our new higher inflation environment. Over the past few years, along with a colleague, we have run this inflation breakeven strategy in an actual portfolio. Recently, we have spoken to ETF providers and ironed out many of the day-to-day details in creating our product. The last step of our journey is finding an institutionally sized partner to seed the strategy.

If you’re a retail investor interested in an inflation breakeven ETF, hang tough — we’ve got our head down and we’re working the puck uprink as hard as we can. If you’re an institutional investor that’s interested in learning more, please contact me at kevin@themacrotourist.com.

Thank you for reading,

Kevin Muir

the MacroTourist

PS: If you are interested in receiving my paid letter, you can subscribe here:

The cost is still $35 USD a month (cancel anytime) or $350 USD if you commit for the full year.

If you want to check out a couple of old posts, here’s a link to a few of my recent favourites:

WHAT’S DRIVING STOCKS

SO YOU WANNA SPECULATE IN BONDS?

WHEN EVERYONE IS BUYING YOU SHOULD BE HEDGING

If you still want to see a few more, send me an email at kevin@themacrotourist.com

And finally, if you are a financial journalist, please send me a note and I’ll hook you up.

Thank you again,

Kev