INFLATION BREAKEVENS: A CORE HOLDING

I have an outlier view of inflation. Contrary to the debt-will-overwhelm-us crowd, I believe the next great financial crisis will not be a deflationary shock, but a return of inflation no one is positioned for. Don’t assume I am a hyper-inflationary doomsayer though. At first the inflation will feel great. It’s not until much later will it actually cause any real problems for the economy.

Don’t bother sending me chuffed emails about how inflation will never return in our current environment of the three D’s - debt, demographics and deflation due to technological innovation. I have heard them all. Your insistence they will overwhelm the financial system will only reinforce my belief that these worries are fully priced in.

And please don’t send me your philosophical arguments about how inflation is immoral and will hurt group blah-blah-blah the worst. You could be correct, but I am not here to decide what should be, rather what will be.

One of these days, society will wake up to the understanding that monetary policy is ineffective at kick-starting the economy and fiscal stimulus will begin in earnest. It will be effective. Too effective. For a variety of reasons it will seem like a free lunch…. at least for a while.

Now don’t get me wrong. It will be abused. Just like monetary policy has been abused (negative rates throughout much of the world is an abomination we should be ashamed of), fiscal stimulus will be taken too far.

Right or wrong, that’s my call. You might debate different points, but I believe a return of inflation is the best long-term macro risk reward trade out there. Hands down. No other trade even comes close to offering this payoff asymmetry.

Yet how do you play it? What’s the trade that will benefit if I am correct?

Although there are a variety of different positions that will perform well in an environment where inflation is increasing, my favourite is long inflation breakevens.

Last month when the deflation-means-all-interest-rates-throughout-the-world-will-go-to-negative-levels bond bulls were pushing fixed-income into rocket-ship-formation-that-looks-more-like-a-penny-stock-promote, I must admit, the pain for bond bears like me was immense. The bond bulls took to twitter to rub salt in the wound and explain why higher fixed-income was a “sure thing”.

However, through the moments of doubt and sleepless nights, in fact, even when it seemed like every single macro-guru and bond strategist was on TV explaining why I was wrong, there was one trade I never considered lifting. I had so much conviction that even amid the darkest day, that period around month-end when the bond bulls took fixed-income to the point of maximum pain, I had the wherewithal to add to the trade. That’s how much I believe in it.

What is an inflation breakeven anyway?

Although many investors understand that TIPS (Treasury Inflation Protected Securities) are designed to offer an investor a way to insulate their bond against inflation, less recognize these securities offer a way to bet on inflation. Inflation breakevens are simply the level of inflation the TIPS market is pricing in over the life of the bond.

For example, here is the US 10-year inflation breakeven:

The TIPS market is predicting an inflation rate of 1.6671% over the next ten years.

The inflation breakeven mechanics

Let’s walk through how these securities work and how you can extract an inflation bet from within.

TIPS are probably one of the most unloved investment classes out there.

Bond bulls don’t want to buy them as usually the whole reason they like bonds is because they don’t think there will be inflation. So why bother hedging for something they don’t worry about?

Inflation bulls don’t like TIPS because even though they are Treasury Inflation Protected Securities, they are still treasury bonds. As such, they still move around with interest rates.

What do I mean by that? Let’s dig into two different treasury issues.

The first is a regular Treasury Bond. In this case, the 3%’s due in 2044.

Notice the face-rippin’ rally at the end of August. That was at the height of the deflationary panic. At that point few believed that we would ever get inflation again. In fact, the overwhelming consensus was that the global economy was about the collapse and you needed protection against deflation, not inflation.

Yet into this panic, what did TIPS do? Well, let’s look at the 1.375%’s of 2044 issue:

It almost looks like the same chart. Wait, why was it going up if inflation expectations were headed lower?

Well, that’s because at their heart, TIPS are still bonds.

Their returns comprise a coupon plus inflation.

We don’t know future inflation, so that part is undetermined. Yet the other part of the TIPS - the yield on the regular part of the bond is known.

For example, here is the yield on that same 1.375% of 2044 TIPS issue over the past year:

As interest rates headed lower, the TIPS yield also headed lower. The key is to realize that TIPS total return = TIPS regular bond portion yield + inflation. Therefore TIPS often move with regular bonds (as we saw this summer).

Although inflation expectations went down, both securities went up. The TIP just went up less (all following charts and calculations courtesy of Bloomberg):

However, it’s important to note that we can isolate that inflation component.

If we know the TIP issue’s yield, and also the yield on a regular nominal bond of similar maturity, we can calculate what the market is expecting in terms of inflation. This is the inflation breakeven rate.

It’s nothing more than the difference in yield between the two different types of bonds.

How to get long inflation

If you wanted to bet on the inflation rate, it would be as simple as going long the TIP security and short the regular bond. If inflation ended up being more than the inflation breakeven rate, then the trade would be profitable. If it ended up being less, it would result in a loss.

There are a variety of different ways to execute this trade. Let’s take our two bonds that we were previously comparing. Although I showed the total return of both bonds, that wasn’t quite the perfect comparison. Due to the higher coupon on the regular bond, it has a shorter duration and therefore to compare the two issues properly, we need more of the regular bond (thus making its outperformance even greater):

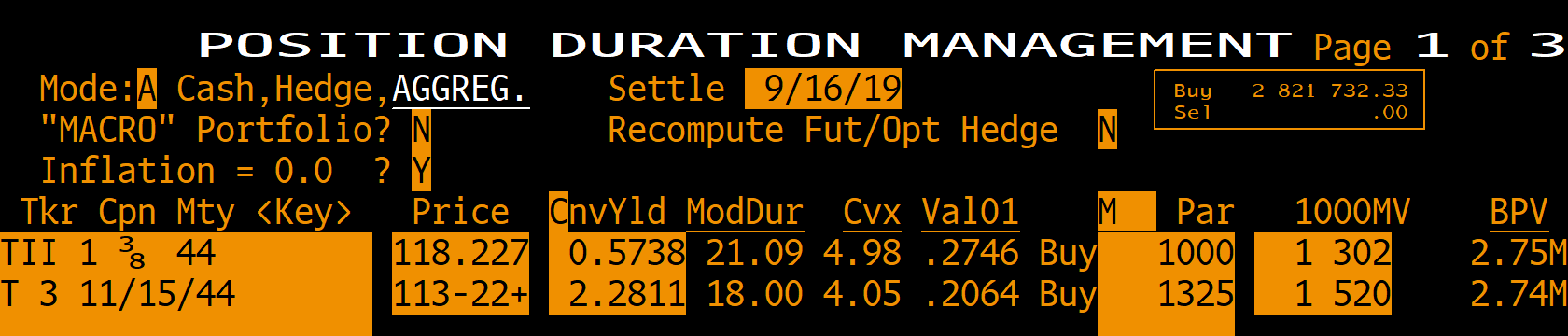

So one way to get long breakevens is to buy 1,000,000 of the TII 1.375% of 2044 and short 1,325,000 of the regular Treasury 3% of 2044. This would give you a “pure” way to bet on inflation over the next 25 years.

However that’s not how I like to do it. I prefer to use futures for my treasury short. On the whole, shorting t-bond futures is more efficient.

Long TIPS short bond futures

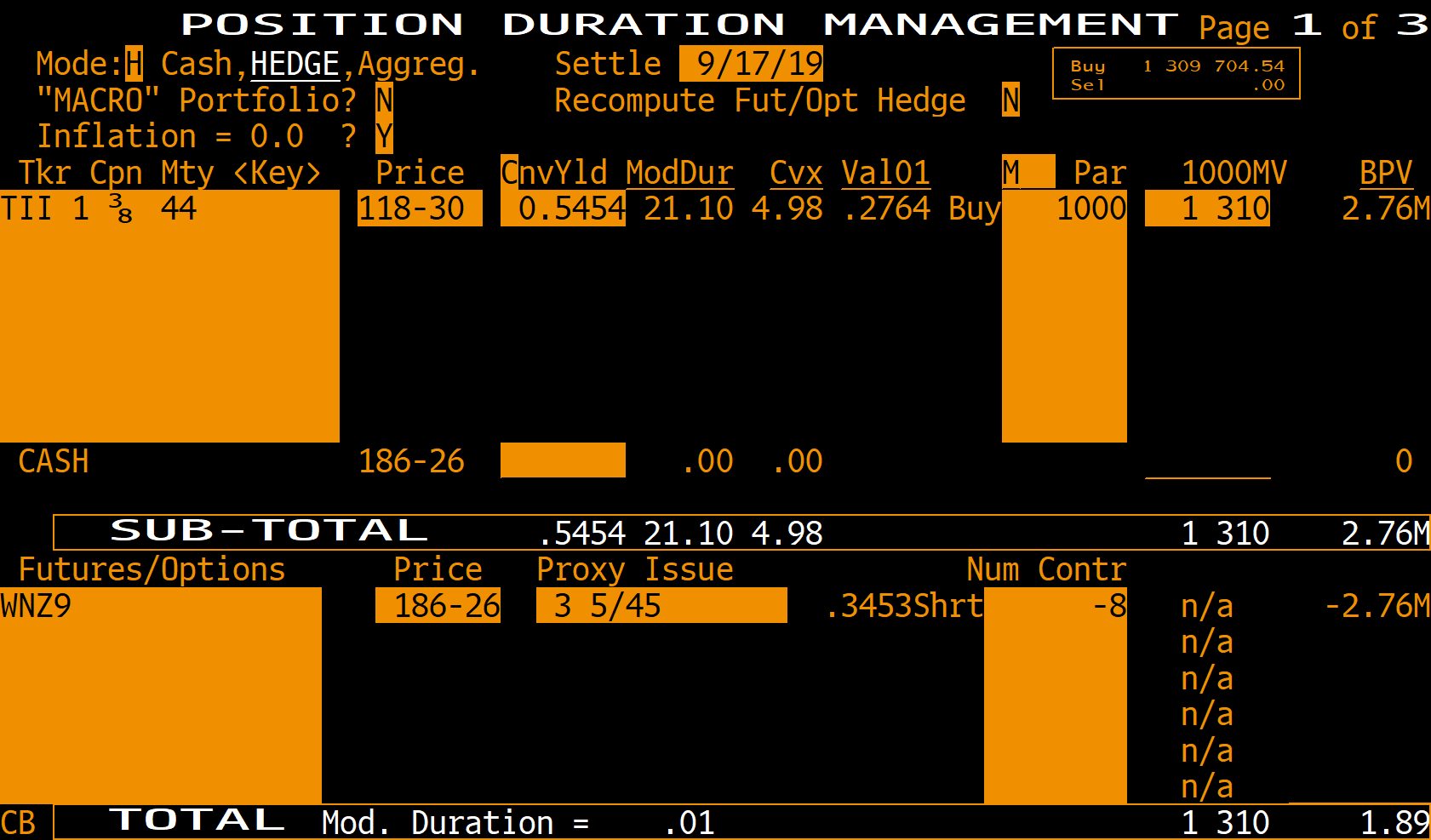

Let’s start with my choice of a 2044 TIPS issue. Why 2044? Why not a true 30-year like the 2049s?

That’s because the ultra-long bond future’s cheapest-to-deliver security is an issue that matures in 2045 and not 2049.

After choosing an appropriate TIPS issue, we need to figure out the relative hedging ratios. Lucky for us, Bloomberg has the handy PDH2 feature.

To get equal positions that have equal BPV (basis point value) change, we need to buy 1,000,000 of the TII 1.375% of 2044 and short 8 ultra-long bond futures (UBZ9 on most systems, but WNZ9 on Bloomberg). Then if all the hedging works out, every basis point of change in breakevens will result in a P&L move of $2,760.

Now many of you are probably saying, “Whoa! That means rolling futures and maintaining hedging ratios. I don’t want that sort of hassle.”

The ETF version of long breakevens

There is another way to get long (or short) inflation breakevens. Before I show you the proper way to do it, I want to highlight the most popular way. Too often I see market pundits graphing the ratio between the TIP ETF and the TLT ETF. At first glance that seems to make sense. Go long the TIP and short the TLT in equal dollar amounts.

But does the math work? And more importantly, how do we go about figuring out the proper hedging ratio?

Well, shorting TLT against TIP makes no sense unless you also want to put on a yield curve steepening bet.

Let me show you why. Here are the TLT portfolio details (all of this is available from the iShares website):

The effective duration of the TLT ETF is almost 18 years.

Now let’s have a look at the TIP ETF:

7.66 years! Ooops! That’s not even in the same ballpark. First of all you would need to use a different hedging ratio to ensure equal BPV. But the real problem is that there would also be an inherent yield curve bet in this spread trade.

What we really need is a government ETF with approximately the same effective duration. And the iShares folks were kind enough to supply us with the perfect product with IEF:

7.57 years is close enough in not only horseshoes, but also for us to use the ratio of the TIP and IEF ETF as a proxy for long inflation breakevens.

So there you go. It’s not how I play it, but TIP/IEF ratio is a great option.

The investing case

There are plenty of investors worried about a repeat of the 2008 Great Financial Crisis. Heck, the hedge fund community seems to make a living warning about the coming crash.

Yet, I ask you; what was the last crisis predicted by the majority of pundits?

I would argue that by its very definition, a crisis occurs because no one is expecting it. So yeah, maybe we get another credit crisis that morphs into an equity collapse with VIX spiking and real estate plunging. But that’s an extremely low probability event. The next crisis seldom looks like the last one.

What “everyone knows for sure but just ain’t so” is the belief that inflation won’t (and can’t) return. It’s what market participants are least prepared for, and what will hurt the most.

Sometime in the next decade TIPS will be manically bid in a desperate attempt to hedge the risk that everyone is so sure is non-existent. That’s why for me, long inflation breakevens are a core holding. It’s one of the few assets that I welcome getting cheaper as it just gives me an opportunity to add to my position at even better prices.

Maybe my confidence is misplaced. Maybe all these deflationists are correct that governments are powerless to hit their inflation targets. However, I am willing to take the other side of that trade. I think governments will figure out how to create inflation, and when they do, it will be too late to buy your insurance.

It’s been a few decades since anyone has worried about inflation. The last portfolio managers and traders who can remember double digit inflation are in the twilights of their career. The fact so few market participants have experienced the pain of double digit inflation is the reason that hedging for that risk is dirt cheap.

I remember wood-paneled station wagons and hearing my folks complain about the rising cost of living. I might not have traded back then, but I have learned that markets have an odd way of reminding market participants there is nothing new under the sun.

Thanks for reading,

Kevin Muir

Most important question : Who are you on the photo?