Yield Curve Surprises

Don't overthink the recent steepening

On Friday, during a holiday-abbreviated session, they took crude oil out back and unceremoniously shot it. WTI futures were down over 5%. Today, with some bad news on the trade-front, the S&P 500 was down over 1.25% in the first decent decline in almost two months.

In this environment what would you expect the yield curve to do? Well, if you would have given me these two data points and asked me to guess the change in the 2/10-year Treasury yield spread, I would have said flatter by 2-5 basis points.

But I would have been wrong. Like Dolly Parton and Sylvester Stallone singing-together wrong.

Instead of flattening, the yield curve has steepened hard during the past couple of days.

Now maybe you will claim this is simply a correction of the latest decline from 27 bps to 14 bps. The 7 bps rally is just a retracement in the bear move. I hear you. On a short-term basis, that's certainly a valid interpretation.

But I like stepping back and looking at the longer-term picture.

This summer, during the bonds-will-never-go-down-again-in-our-lifetime scramble, bond bulls flattened the curve below 0 bps. The shrill calls about the oncoming recession due to the yield-curve-inversion signal caused even more purchases of long-dated bonds.

However, since the first day of September, the yield curve has steadily steepened. And here we are in December, with every reason to flatten the curve, yet what happens? It gets pushed higher.

When a market doesn't do what it's "supposed" to do, and when a big group of speculators get caught pushing a position too far (like this summer's bond reach), I pay attention.

The bond market is giving hints that surprises will be on the dark side. I continue to love the steepener trade. Today's action confirms the trend continues to be higher (a steeper yield curve). Don't overthink it.

Thanks for reading,

Kevin Muir

the MacroTourist

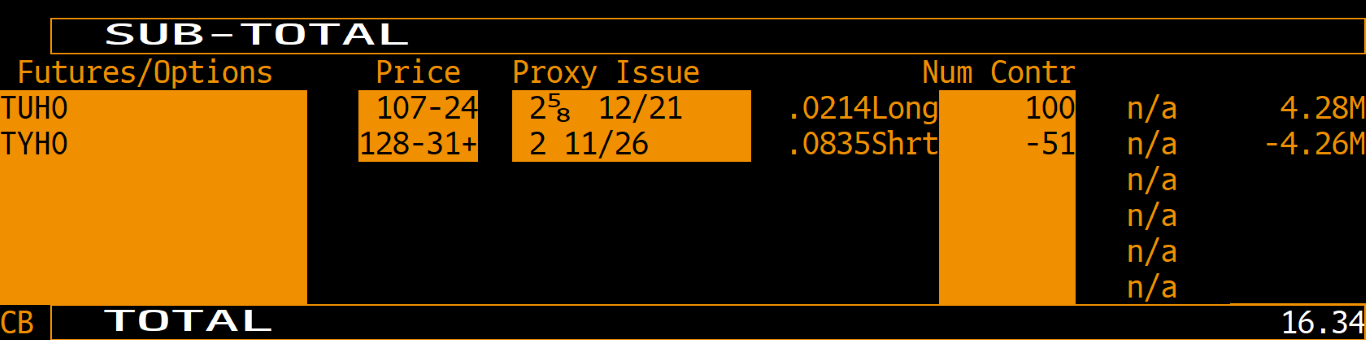

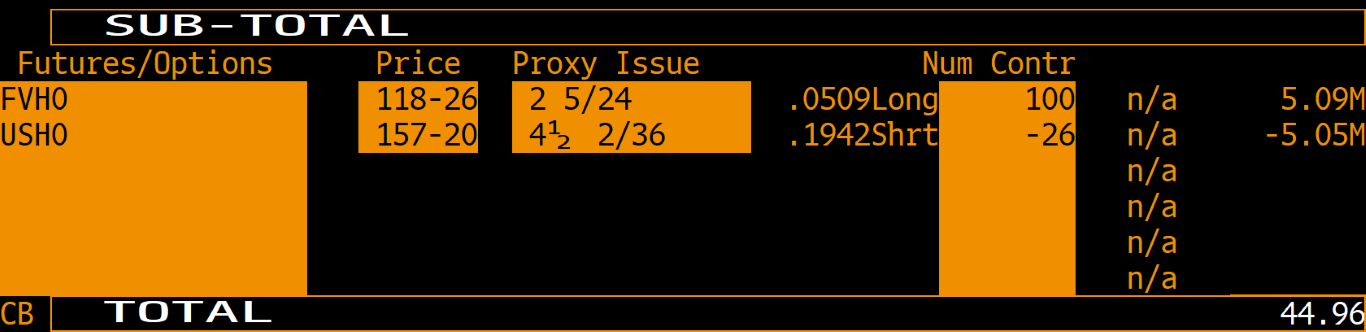

PS: For those interested in the March future hedging ratios, here are the 2/10 and 5/30 calculations.