WORRIES ADD UP

As many of you are aware, I am usually an equity bull. Let’s face it, over time, stocks often rise and it’s difficult to fight that tendency.

Yet the trader-in-me believes the time to lean against this propensity is upon us. I have abandoned my US long equity positions, and am leaning short on a trading basis.

Why the shift in tone? Let me sketch out the worries that have finally overwhelmed my desire to stick around for the last innings of this party.

Yardeni’s hint

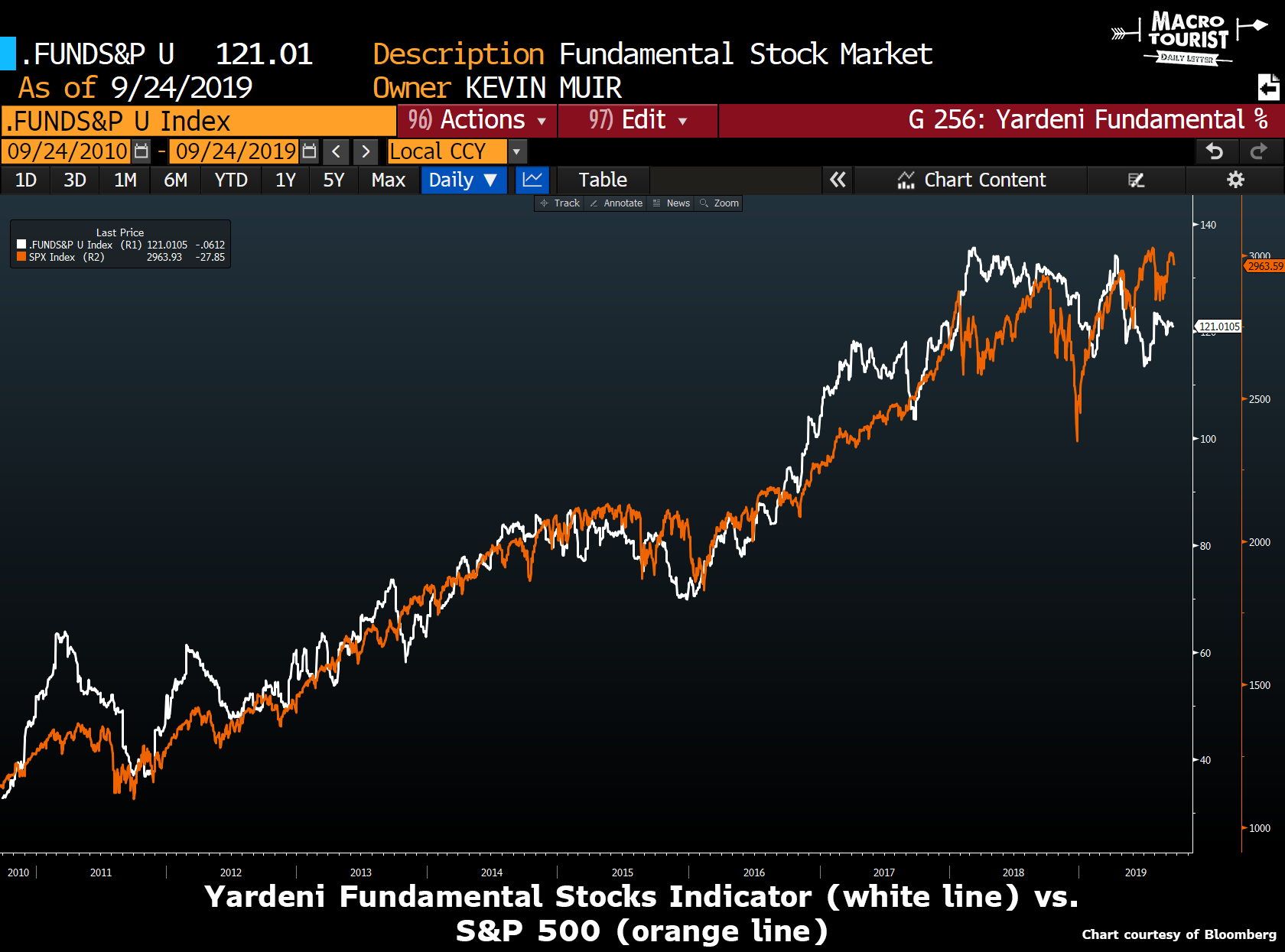

One of my favourite indicators is Ed Yardeni’s “Fundamental” Stock Indicator. I have written about it in The Best Unknown Indicator and Obi-Ed’s Magical Indicator so there is no need for me to rehash all the details. Needless to say, I have learned the hard way not to disregard this signal. When either series diverge, it seems like it’s only a matter of time before they converge again.

Even though the S&P has been pushing to new highs, Yardeni’s indicator refuses to join along. Why is that?

Well, the indicator has three main inputs - employment, consumer confidence and CRB Raw Industrial commodities.

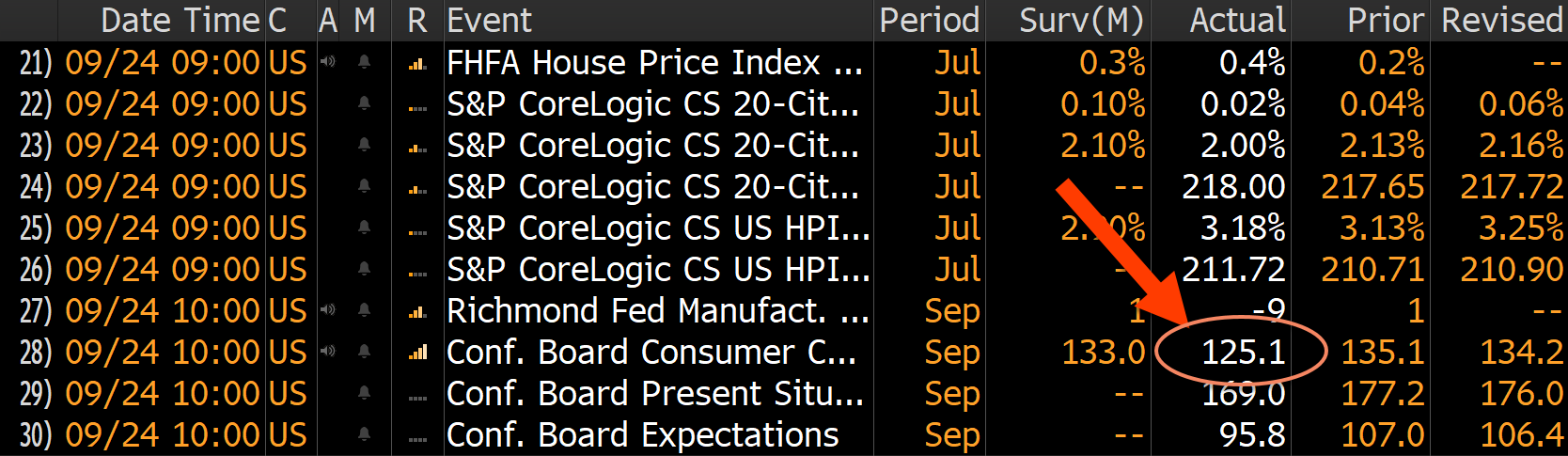

Initial jobless claims have been well behaved and show no signs of faltering. Consumer confidence had been resilient, but today’s release showed the first potential cracks.

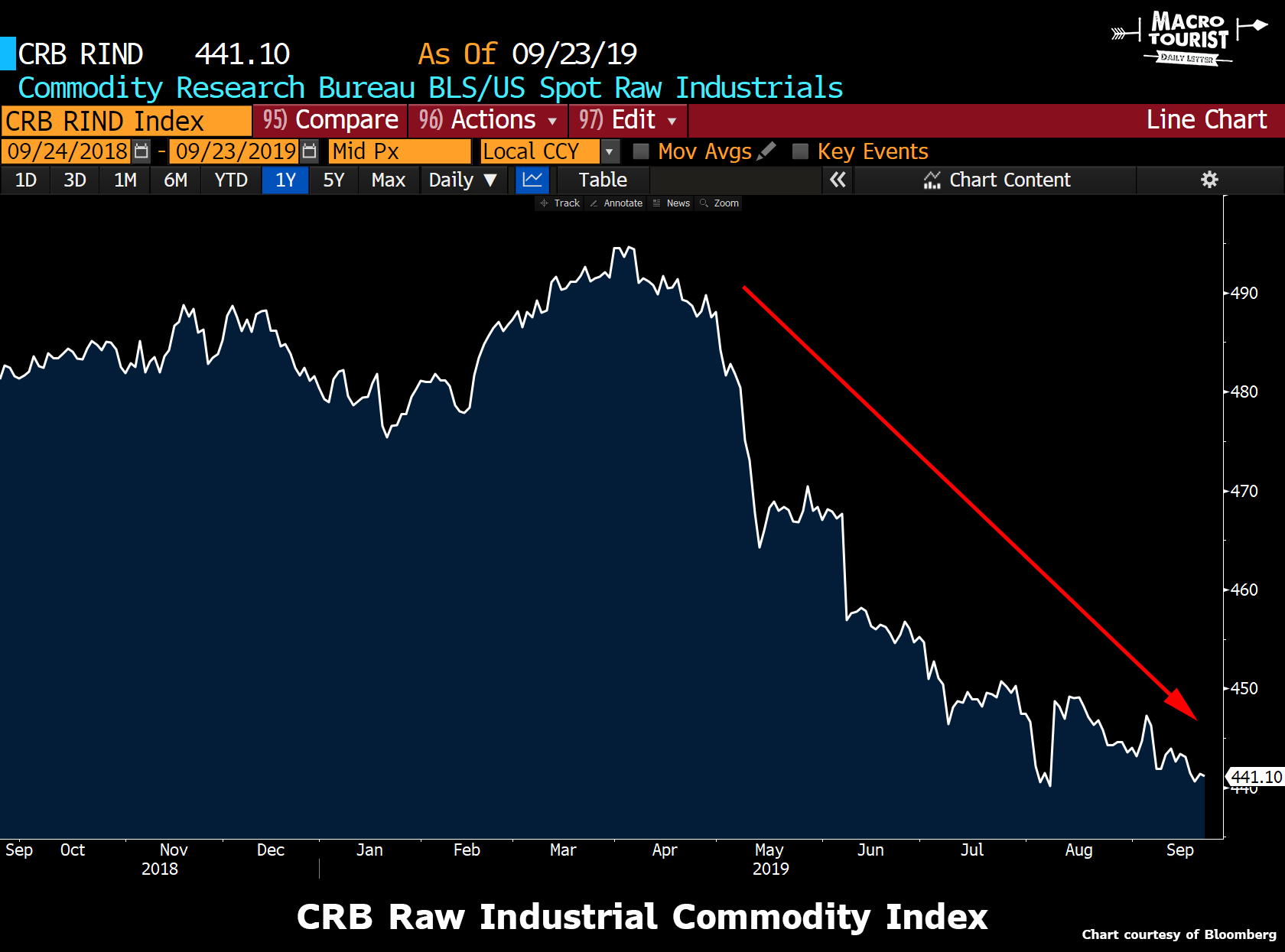

But what has me most worried is the CRB Raw Industrial Commodity Index.

These commodities represent the building blocks of the global economy. It’s tough to get robust economic growth with the CRB Raw Industrial Commodities Index bumping along the lows.

Without a rally in this index, I don’t see how Yardeni’s indicator moves higher to close the gap, and therefore I worry that it resolves with the S&P 500 heading lower.

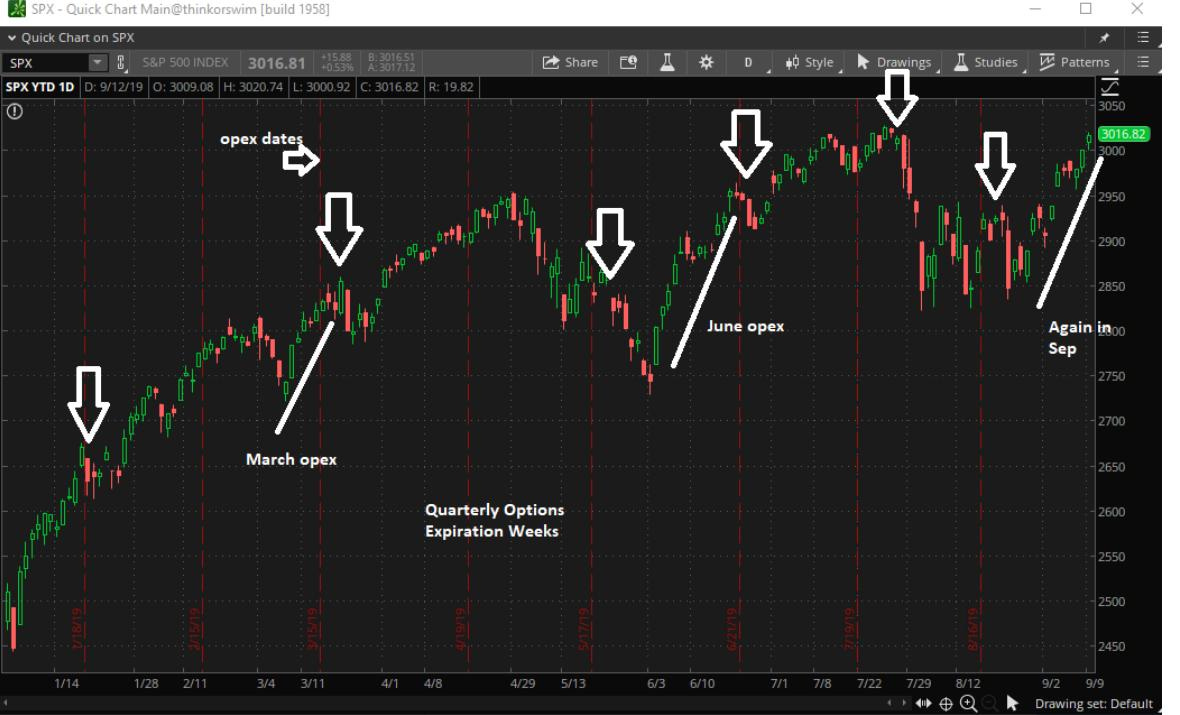

Seasonal triple-witching expiry weakness

Next up in my list of worries is the fact that we have just passed a triple-witching quarterly expiry - a point of time that has lately often been followed with stock market weakness. Here is a great chart by Scott Murray of @VolatilityWiz fame which highlights the S&P 500’s tendency to run up into expiry and then fade in the next week or two.

This September saw a near perfect setup. We rallied into expiry and are now threatening to roll over.

Repo-steria

Last week all sorts of shenanigans occurred in the repo funding markets. I will not bother giving you my opinion about the reasons for the stress. Yeah, I know the argument that it’s not a big deal as the Federal Reserve was able to provide the liquidity the market was needing.

But I worry about why they needed that liquidity. What changed in the financial system to cause that sudden need?

Sure, you can tell me about the big tax payment or the bombing in the Mideast, but we have had plenty of issues for the past nine years and there was no need for the Federal Reserve to do special repo operations. Now all of a sudden, they need to provide liquidity.

Could it be nothing? Of course. Heck it could even mean that liquidity is being used for more productive stuff. But I worry there is too much hubris on the Fed’s part. I worry that just like the recent yield curve inversion, they are busy coming up with reasons why this time is different.

This great picture was captured by Chris Whalen with the line about “we’ll see how this one ages.”

I worry that we will look back to this week’s funding stress and say that the signs were there, but we ignored them.

Geopolitical tensions

I am writing this in the aftermath of Trump’s speech at the United Nations. I am surprised the markets didn’t react even more violently to his comments. They were about as hawkish as I have ever seen. Whether it was the Chinese or the Iranians, I just don’t see the geopolitical situation getting better before it gets worse.

The market is underestimating the potential risks. The stock market has become numb to all the rhetoric, but I worry one of these days, it will turn into something more ominous than just words.

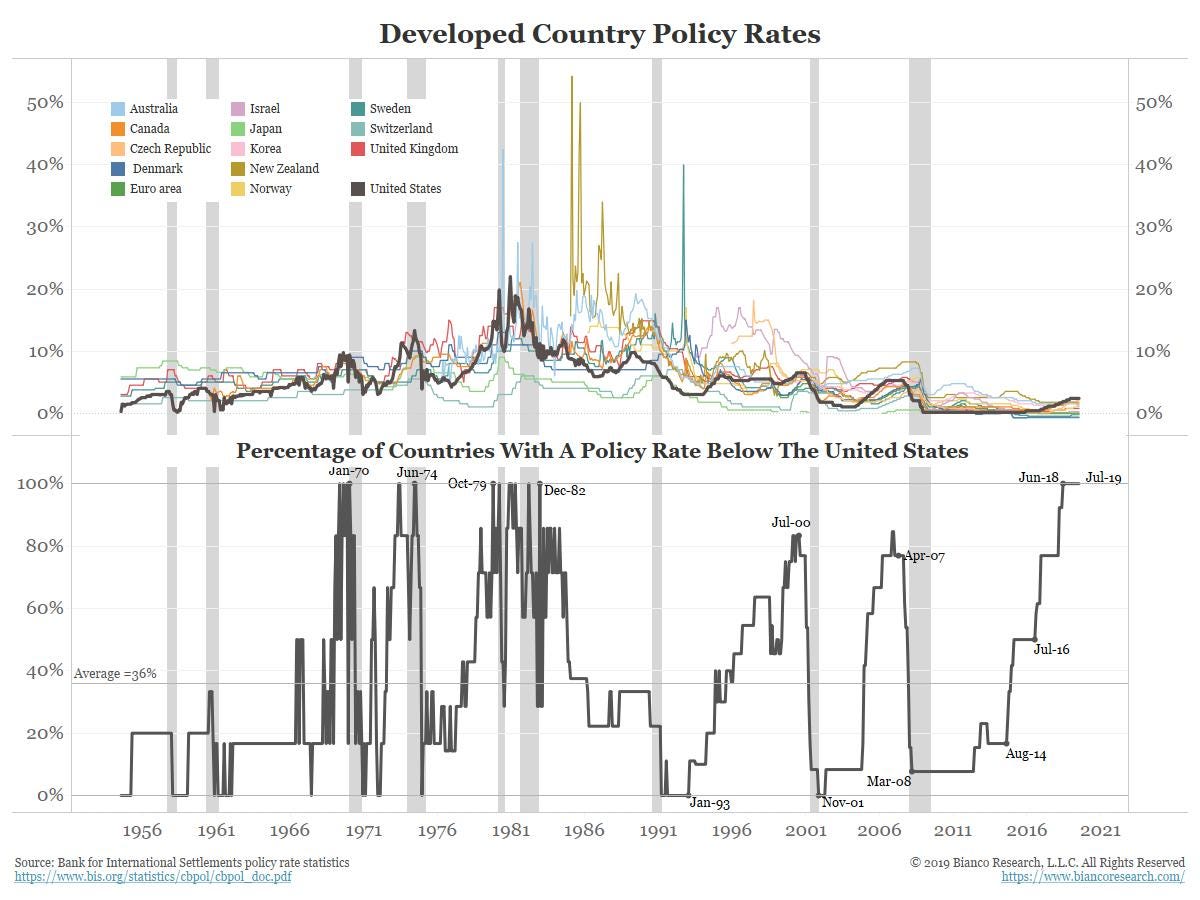

The biggest problem out there

And want to know my main worry? The country with the world’s reserve currency has the highest policy rate out there in the developed world. If we look back over time, this has often coincided with market crises.

I call this next graph, “The Most Important Chart in the Whole World”. It’s by the great Jim Bianco at Bianco Research and I have become a little bit of a zealot about it.

It sums up the main problem - the US is too tight for the world economy.

Now please don’t send me arguments how it’s the rest of the world’s fault for being too loose - I completely agree! Just like the United States, the rest of the world should implement fiscal stimulus and stop relying on monetary madness.

But our job is not to decide what should be, but calculate what is. And with the Fed so tight relative to the rest of the world, eventually it causes problems. Big ones.

Not turning into an uber-bear by any means

Don’t misunderstand me. I am not turning into one of those the end-of-the-world-is-upon us bears. Yet I think the time to be heavily long is past. The next 5-10% in the stock market is more likely to be down than higher.

Time to lighten up and look for spots to take stabs on the short side.

Thanks for reading,

Kevin Muir