WISDOM FROM CARL THE JANITOR

It was 35 years ago this weekend that five high school students met for all-day detention at Shermer High School.

With three teenage children at home, the MacroTourist has sat through more than his share of adolescent movies, yet apart from a couple notable exceptions (Easy A and The Perks of Being a Wallflower spring to mind), few movies even come close to the greatest teenage movie of all time - John Hughes’ masterpiece - The Breakfast Club.

Often when I dust off an old movie it fails to live up to the idolized version in my mind, but not so with this classic. And as I recently re-watched the final scene, I was struck by wisdom in those last few lines.

Dear Mr. Vernon

We accept the fact that we had to sacrifice a whole Saturday in detention for whatever it was that we did wrong. But we think you are crazy to write an essay telling you who we think you are. You see us as you want to see us. In the simplest terms. The most convenient definitions. But what we found out is that each one of us is a brain, and an athlete, and a basket case, a princess and a criminal. Does that answer your question?

Sincerely yours,

The Breakfast Club

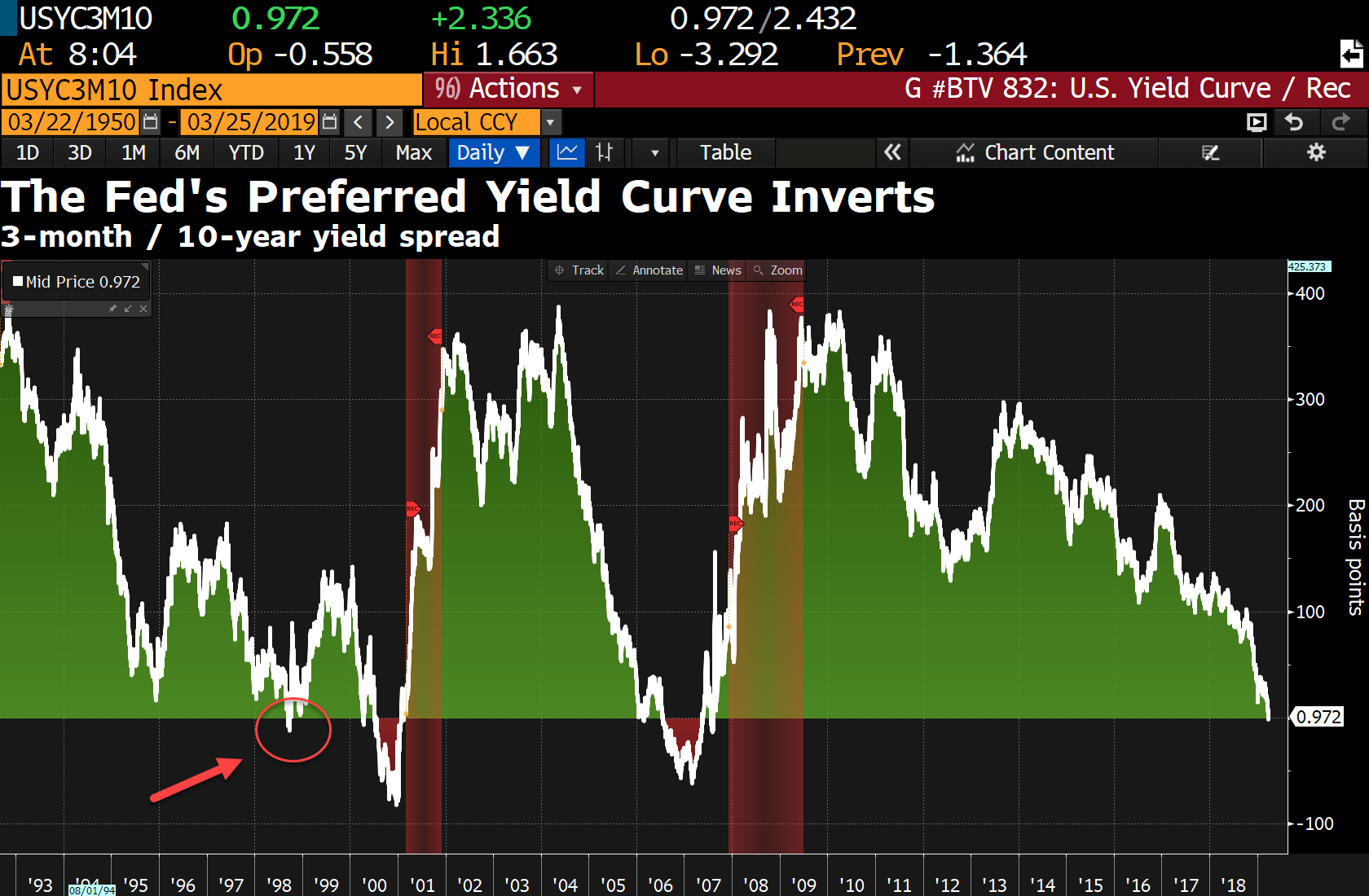

Late last week, the 3-month t-bill versus 10-year treasury note yield spread inverted, and with it, came all sorts of dire predictions of the imminent catastrophic collapse that this was signaling.

But could it be that the market was making the same mistake as Principal Vernon? Was the market seeing this information as they wanted to see it? In the simplest terms and most convenient definitions?

I am aware of the historical accuracy of the yield curve in forecasting recessions. Let’s face it, the yield curve has a better track record than most economists.

And there are plenty of smart strategists warning about the dangers of claiming “this time is different” and trying to reason away the yield curve inversion. David Rosenberg and Raoul Pal are two such individuals who immediately pop into my head.

Well, I am going to politely suggest that maybe this time is indeed different. I know, I know. I was trying to figure out a way to couch this without uttering those most expensive four words in the investing language. Who wants to be the idiot going against history and iconic market strategists? It’s almost a no-win-scenario. As I write it, I look like a knob who doesn’t understand market precedent, and if I am correct, no one will remember. It’s such a better risk-reward in terms of reputational risk to join the chorus of bears who believe the Fed’s recent flip-flopping is due to some sort of grandiose understanding of the inner workings of the global economy. You just seem smarter arguing that side.

These bears who were screaming you should sell stocks because the Fed was too tight are now howling that you should sell stocks due to the Fed’s dovishness - it seems like no matter what the reason, you should sell stocks.

The yield curve is inverting because the market is increasingly pricing in an easy Fed, but it might not be because of a collapsing economy, but rather a capitulating FOMC Board.

Over the past week the 3-month Eurodollar futures contract has priced in more than 30 extra basis points of easing over the next two years.

This has happened as the stock market has been screaming higher!

The reason I am so willing to say this time is different is because we have never had this sort of dovish flip-flop from the Fed not in the midst of a crisis.

When Powell succumbed last December with his abandonment of “we’re a long way from neutral” comments, almost no one would have dreamt that he would run so far to the other side of the boat so quickly. This has been an unprecedented dovish shift from a Fed.

At last week’s FOMC Board Meeting, expectations were fairly high that Powell & Co. would continue with their easy ways. Yet they somehow managed to find a way to exceed already-heightened expectations of easier policy.

Although the bears will take that as a signal something sinister is lurking in the global financial system, what if the Federal Reserve has simply resigned to Trump’s desire for easy monetary policy? What would wholesale desertion of prudent monetary policy look like?

I humbly suggest this is what we are witnessing.

The Federal Reserve has decided it no longer wants to be the last adult in the room holding back the financial excesses and has relented to let the economy run hot. The Neel Kashkari wing of the FOMC has won out.

So when the bears look at the recent inversion of the 3-month T-bill versus 10-year Treasury note yield spread and pull out their risk asset pink tickets because it looks an awful lot like 2000 and 2006, I say “Whoa. Hold up. What about 1998?”

Remember back to that year? The Federal Reserve was facing a crisis from the collapse of Long Term Capital Management. The S&P 500 has declined 22.45% in a scary summer swoon.

Then the Fed rode in to the rescue, eased policy, and risk assets took off like they stole something.

It’s pretty pathetic, but last December’s decline seemed to have scared Powell’s Fed as much as 1998’s LTCM crisis.

The decline wasn’t as large as during the LTCM crisis, but the 20% was all it took for Powell to see the wisdom of no longer fighting Trump’s wishes of easy monetary policy.

Although the yield curve inversion may signal economic recession is right around the corner, it doesn’t necessarily have to.

It could be that this dip towards zero ion the yield curve ends up just like 1998.

Could I be wrong and might the Fed have raised rates too hight too quickly and these adjustments proves to be too little too late?

You betcha!

Yet, I have to ask the bears if the price outcome for risk assets is predetermined? Can the Fed do nothing to alter their trajectory? And assuming there is a level of monetary ease that can resume their northward course, how much easing does it take?

Does the Fed have to actually cut rates before you get bullish? Surely there has to be some level of monetary madness where you throw in the towel and agree that risk assets will continue their ascent due to monetary stimulus.

I am not sure if the Fed’s flip-flopping is enough to send stocks screaming higher in a 1999 style melt-up, but I can tell you one thing for sure, I am not nearly confident enough to dismiss this possibility either.

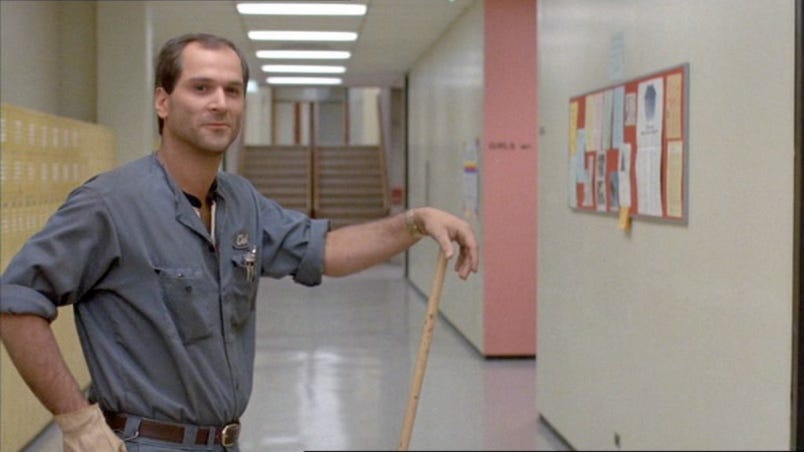

The bears that keep moaning about the insanity of the Fed’s policies but insist on fighting the market with short sales remind me of Principal Vernon complaining that the kids have changed.

VERNON: Carl don’t be a goof! I’m trying to make a serious point here. I’ve been teaching, for twenty-two years, and each year these kids get more and more arrogant.

CARL: Aw bullshit, man. Come on Vern, the kids haven’t changed, you have! You took a teaching position, ‘cause you thought it’d be fun, right? Thought you could have summer vacations off and then you found out it was actually work, and that really bummed you out.

Maybe the market hasn’t changed either. Maybe this is just 1998 all over again. We all get older, and maybe we should all try to be as wise as Carl the janitor.

Thanks for reading,

Kevin Muir

the MacroTourist