WHEN A BUBBLE BURSTS, EVERYONE LOSES

And the 'tourist's plan to prove his pal wrong

I am fortunate to count some wise traders as friends. You know the type; folks who have managed money, and even more importantly - other traders, for decades. They are savvy because they have made (or seen) every mistake in the book.

I remember having a discussion with one of them about my foray into shorting what I believe to be the biggest bubble of my lifetime. I’ll leave you to guess which asset. The specifics of the trade don’t matter.

What’s important was his comment that “when a bubble bursts, everyone loses.”

What did he mean by that glib remark?

Although it’s easy to look at past bear markets and imagine the money that could have been made shorting, sticking with that trade is insanely difficult. Way more than most investors realize.

What many forget is that the strongest short-term rallies don’t occur amid bull runs, but are instead peppered within painful bear markets.

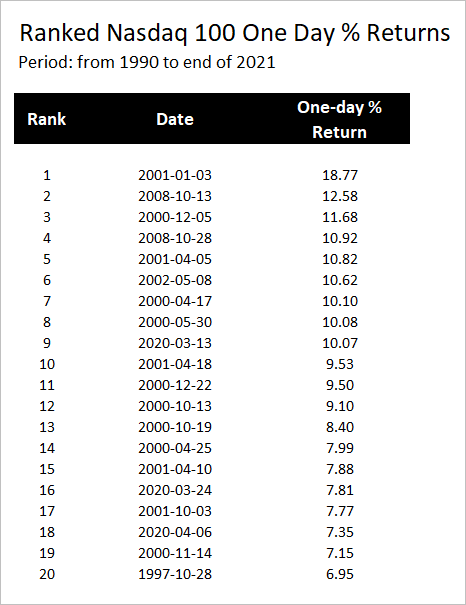

To prove that point, I created a table of the largest one-day percentage returns for the Nasdaq 100 index over the past 30-years.

Look closely. Those dates aren’t the start, middle, or even end of bull markets. Nope. Those dates are almost all sprinkled within the ugliest bear markets.

This is why trading from the short side is so difficult.

My favourite character in Michael Lewis’ classic Wall Street novel was always the human piranha (that’s what happens when you read it first as a nineteen-year-old).

Although the piranha’s language was juvenile, there is probably no better environment to get your face ripped off than a relentless bear market. It is the perfect description of what happens to the shorts.

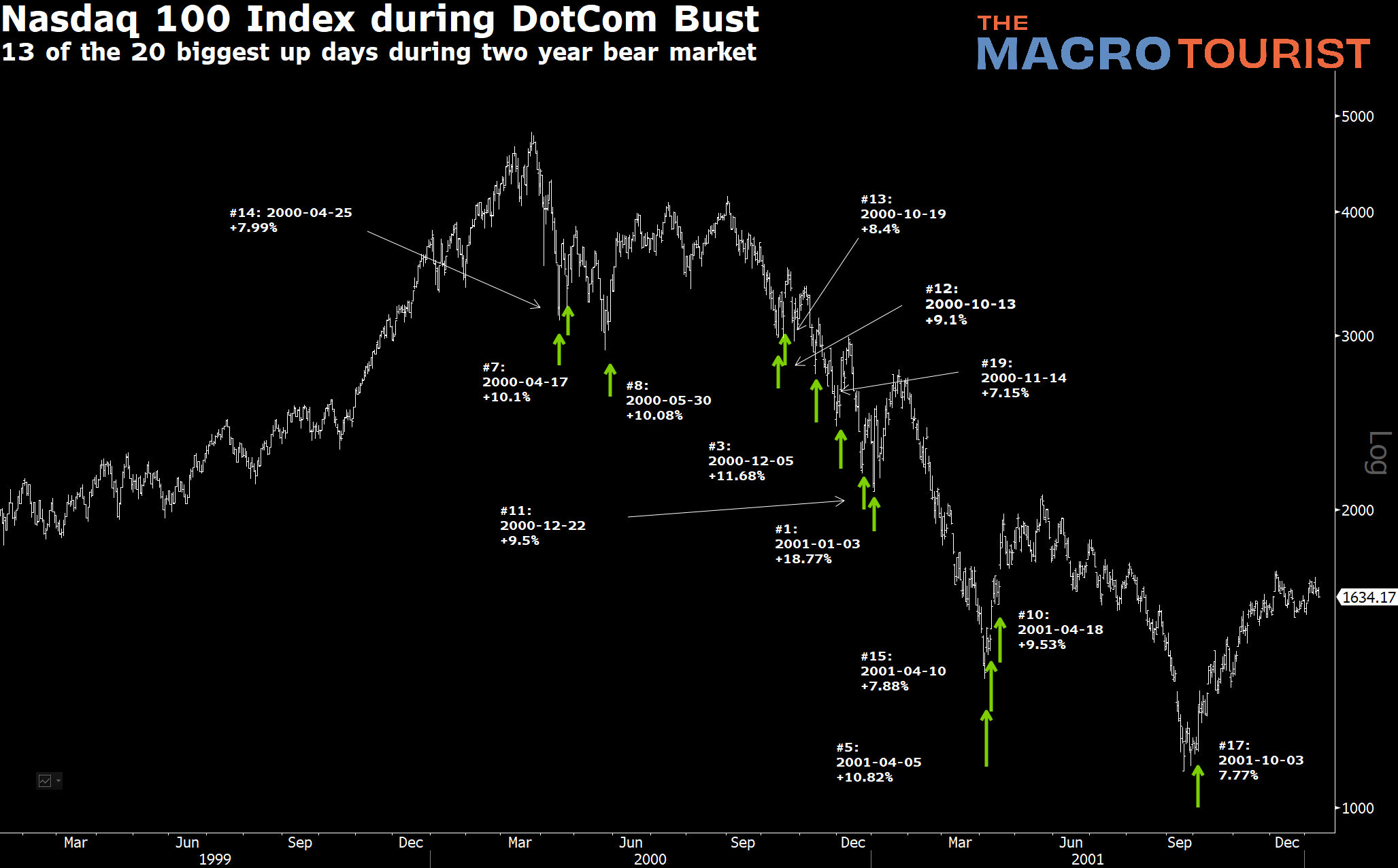

Let’s examine what was probably the best short-side-trading opportunity of the past few decades - the DotCom bust.

From 1998 to 2000, the Nasdaq 100 Index went from approximately 1,000 to 5,000.

Then, from 2000 to 2002, it went from 5,000 back to under 1,000.

Shorting that index must have been like getting out a shotgun, aiming at the bucket of fish, and squeezing the trigger. Right?

Well, let’s have a look at the decline. But instead of only showing a nice chart that goes from the upper left to the lower right, I have highlighted all the “top twenty largest single day rallies in the Nasdaq 100”.

Sometimes it is difficult to see the details, so I have created a larger version for download if you are interested.

During the DotCom bust, there were over 13 times when the Nasdaq 100 rallied anywhere from 7.77% to 18.77% in a single day!

As I write this piece, the Nasdaq index is trading at 15,600. A rally today equal to the previous largest gain would equate to almost 3,000 points! I don’t think even Michael Lewis could dream up enough copulating inanimate objects to describe that level of face ripping.

This explains my wise pal’s comment that when a bubble bursts, everyone loses; the bulls refuse to sell (and often keep buying), and the shorts end up getting squeezed out during violent rallies.

The ‘Tourist is going to try anyway

I refuse to accept that no one can win during a bursting of a bubble. Chalk it up to my stubborn desire to master this investing game.

But it requires a change in tack.

As you folks know, I have been quite bearish on tech - especially the most speculative kind. For some time now, I have argued that the “bull market in crap is over”. My suspicion is that many of these “dream and meme” tech stocks will end up having charts similar to the Nasdaq 100 DotCom bust. However, think about what that means. Many will have rallies that rip the shorts’ faces off.

We need to be ready. We need to expect 10-20% up days.

We also need to make another change. Instead of shorting when things look like they are breaking down, we need to alter our strategy. We need to sell hope, and cover into despair. The reason there are such violent rallies is that everyone sells at the same time. Longs puke into the hole and shorts jump on board. Inevitably, it gets pushed too far, and then the shorts get nervous. The stock explodes higher. Even though, at this point, it might seem like the bear market is over, that’s rarely the case. These rallies-filled-with-hope are just opportunities to pull out more pink tickets.

In practice, this means that the more bearish everyone gets, the less confident you should be about your short trade. But, please don’t misconstrue this to mean that playing for a bounce in these names from the long side is a good idea. Nothing could be further from the truth.

The purpose of this piece is to remind you that bear markets have the most violent short-term rallies. We should strive to trade in a manner that enables us to sell into strength, as opposed to covering into the scramble. Even though my buddy tells me that everyone loses in this type of environment, I’m going to prove him wrong. Or at least I’m going to try.

Thanks for reading,

Kevin Muir

the MacroTourist

Kevin, glad you mention that violent rally happens in bear market. It's the same thing in SPY. When SPY jumps more than 3% in one day, it is a confirmation that we are in a bear market.

This is where I like to use put spreads. Doing it as a spread minimizes paying crazy vols outright as you're spreading one vs. the other (buying ATM or OTM and selling further OTM), and reduces your theta decay. You don't get the vega pop of outright puts, but if your alternative is shorting delta 1, then it's not much of a loss. Then on the crazy rallies, your delta goes away making it a whole lot less painful. I don't trade the asset that shall not be named, but if I did trade it from the short side, I'd take a hard look at put spreads as a risk-managed way to do it. Just my 0.02.