WEEKEND COLOUR COMMENTARY

For the weekend of 2019-11-30

This week's recommended twitter account

Dylan Grice, former SocGen strategist has re-emerged on twitter, and not only that, he is writing a free monthly piece.

His twitter account is accessible here and although you should really sign up for his research by clicking here, I don't think he would mind me linking to this month's article for you to get a feel for his writing.

My Favourite Podcast this Week

What do you get when you mesh two great reporters with the resources of the Bloomberg media team? One of the best financial podcasts out there.

I rarely miss Tracy and Joe's OddLots Podcast. They do a terrific job making professional financial topics fun and still extremely enlightening.

I am recommending two specific episodes:

"Why the Repo Markets Went Crazy" with Zoltan Possar and "The Great 'WhoDunIt' of Taiwanese Life Insurers" with Brad Setzer. Take the time for both of these. You won't regret it!

My article about the Canadian yield curve generated a lot of comments. Some positive, lots negative. Most of the pushback was... cordial. You might even call some of it helpful. Like the following; Louis Gave of Gavekal Research was kind enough to take some time to discuss why he thought Canada would be a benefactor of the coming inflationary pulse. I'll let him sketch out the argument:

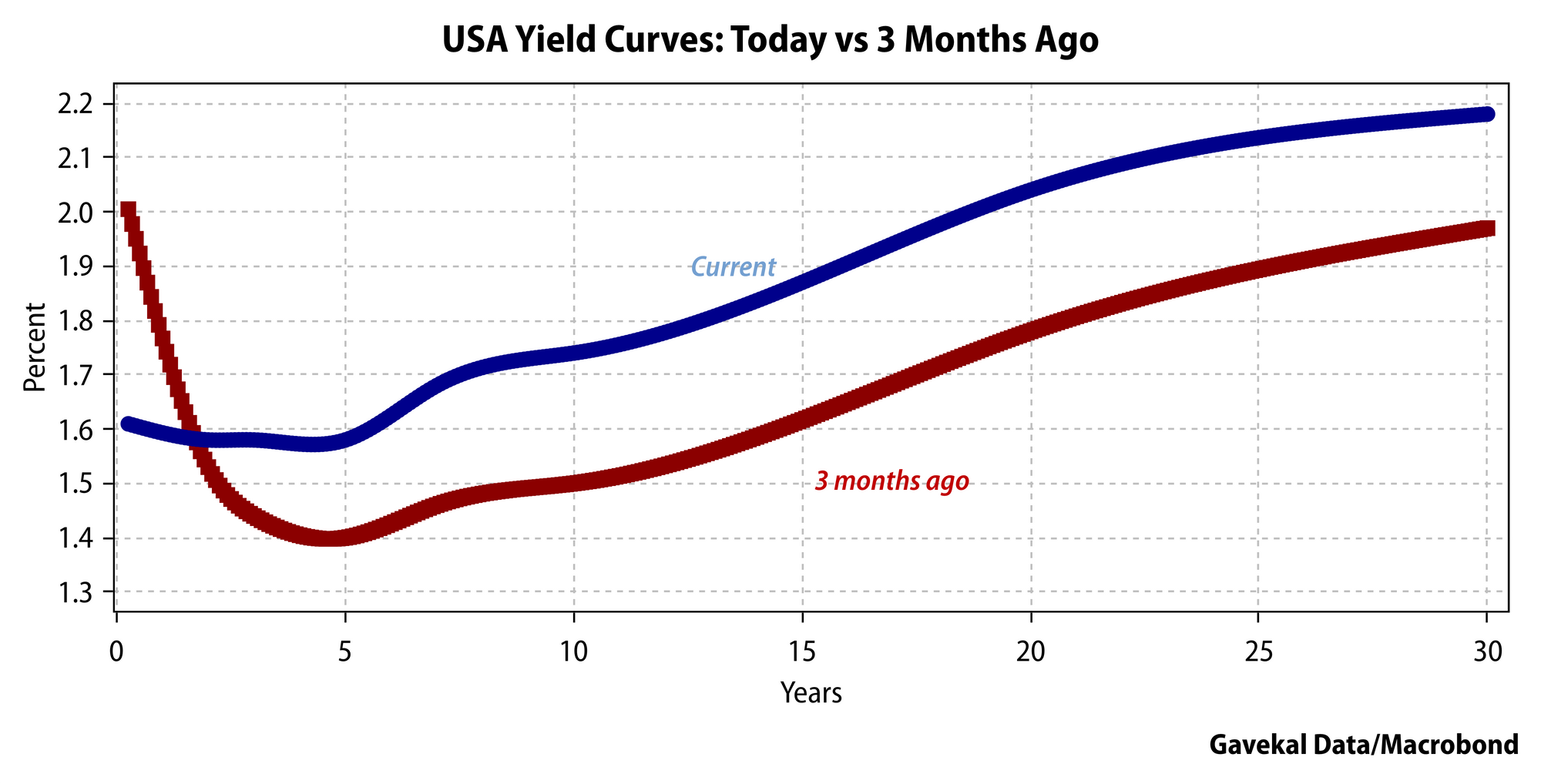

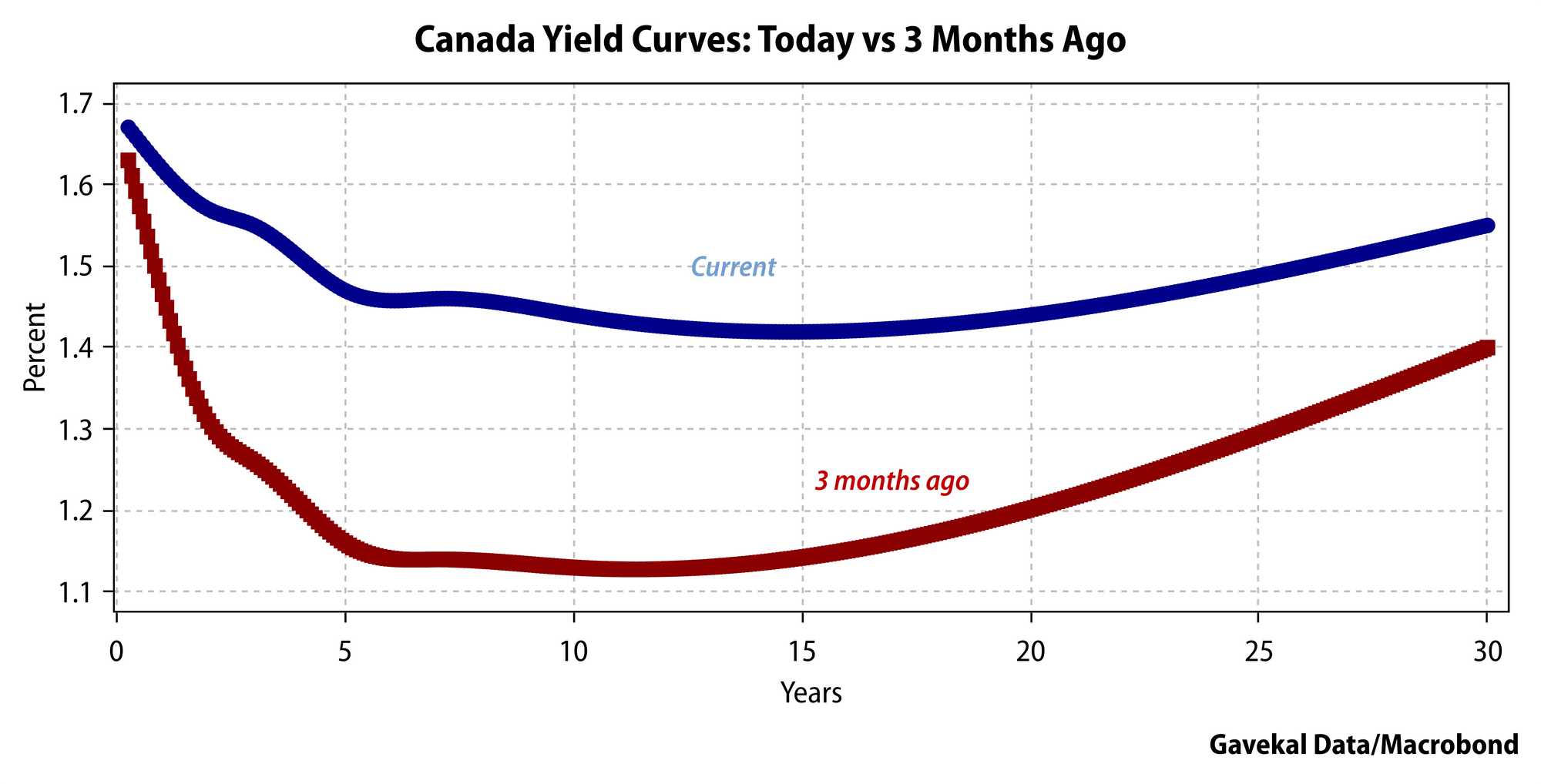

Thank you for the piece. A lot of food for thoughts. I am not sure I come to the same conclusions as you do though. First, a look at the US and Canadian yield curves, now and then three months ago.

So the long end on both sides have come back roughly 30bp, give or take. The main difference is at the short end, where the Fed has cut interest rates and the Bank of Canada has not.

Now I guess that your argument for Loonie bearishness is that the Fed having cut rates, the Bank of Canada will have to follow, and that once the Bank of Canada cuts, then the loonie will fall?

But then, when I look at the evolution of the curves, it seems that the Canadian bond market was screaming for a cut MORE three months ago then it is today. I mean, three months ago, the Canada 2 year was at 1.3%. Now it is at 1.55%. If you are the Canadian central bank, surely you are more likely to be more ‘relaxed’ about your policy stance when the two year is getting closer to your short rates then when it is very far away?

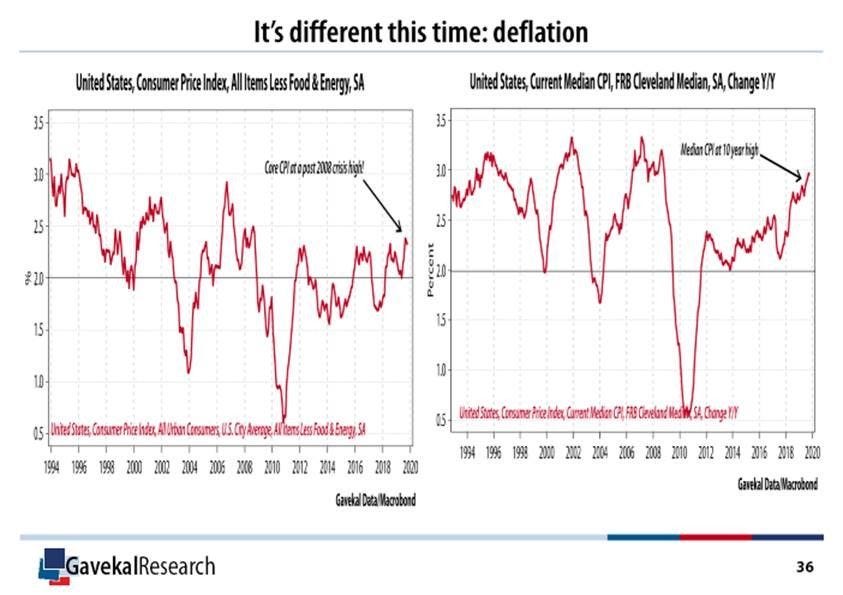

Taking a further step back (much further back), I happen to agree 100% with your view that the market is massively complacent about inflation. As things stand, USA core CPI is at a 10 year high, Unit Labor costs are rising 2.5% per annum and median CPI is at 3% (see charts below). And this IN SPITE of a strong US$, weak global manufacturing, lackluster growth and energy prices that remain contained. What happens if, in a year from now, the US$ is weaker + energy higher (it could happen!). Where will median CPI be: 4%? 5%?

Which brings me back to your CAD bearishness: in a world where the REAL RISK to financial markets is inflation, WHY would I want to short a commodity currency? And why would I want to short the one currency managed by the one central bank that didn’t wet itself when yield curves inverted? Why would I want to short the ONE G7 currency from the ONE central bank that doesn’t think QE is the end all be all?

After all, today, we have the Fed cutting interest rates and embracing QE (I know that the Fed doesn’t want to call it QE. And I know that we live in the 21st century and that if a Fed debt monetization program wants to self-identify as non QE, we should be respectful of that choice. Still, I am old-fashioned and non PC, so I will call this QE anyway!) at a time when:

1. Core CPI and median CPI are at a decade+ high.

2. Unemployment in US, Japan, Germany and the UK are at all time lows. There is no good data on Chinese unemployment but labor market there is decently tight as well.

3. Stocks are at all time highs.

4. Budget deficits at both local and federal levels are sky-rocketing (and let’s not kid ourselves that the Fed restarting QE is not 100% driven by the need to bankroll the various arms of the US government)And I would want to be long the US$ with this?

If the Fed behaves this way when all is hunky dory, how will the Fed behave when the train gets off the tracks? It will absolutely SLAUGHTER the US$, that’s what it will do!

And that’s before you even go into the ‘Warren risk’ and the general gong-show that US politics are offering (say what you will about the British parliamentary system, at least it has the great benefit of running just 6 weeks campaign so we don’t have to see the Trudeau/Corbyns of this world for very long).

Anyway, given all of the above, and the greater uncertainty of the world that we live in (see attached), I will take my currencies with the Queen’s head (UK, Australia, NZ, Canada…). I’ll leave you the green stuff!

Yours truly - Louis

After some great back and forth, I realized that Louis and I were more on the same page than not. Especially when he left me with this email (that definitely made me laugh and appreciate Louis all the more):

I guess if we go through the main Canadian growth drivers:

Real estate: now been struggling for past two years or so (at least looking at the Toronto and definitely in Vancouver)

Autos: its been a bloodbath globally… but could it be bottoming?

Mining: Been a bloodbath… but could be bottoming?

Energy: Been a bloodbath… but could be bottoming

Farming: sucks structurally as a business but could actually be benefiting from China’s need to import massive amounts of food (to get 3.7% CPI back down)

Aeronautics: the Boeing 737 Max has been a shock that no one expected and wrecked havoc on many a company’s order book… however, this could be coming to an end?In short, none of the Canadian business lines feel very ‘toppish’ to me. Most have been consolidating for past few quarters.

I won’t argue your point that Canadian policy makers are nincompoops. Still, if the Green-NDP alliance loses power in the next regional election in the People’s Democratic Republic of British Columbia, then the liberals are back in and we will likely see the pipeline to Prince Rupert that Alberta so clearly needs…

Anyway, time will tell. But when it comes to positioning, it seems to me that:Everyone and their dog hates on the Loonie, the Aussie, the NOK etc…Everyone and their red-haired cousins hates on the EuroEveryone and their first wives hates on the RMBEveryone, and I mean REALLY everyone, LOVES on the US$

Meanwhile, where you have the biggest potential for disappointment is precisely the US$.

Thanks for writing Louis. I appreciate you sharing your points of view with myself and the readers!

My article also had lots of comments on twitter. It seemed like the Canadians were more sympathetic to my argument, while the rest of the world was busy telling us how great everything is (and will continue to be) in Canada. However, one loyal reader rightfully pointed out that when measured by the return of our stock market in US dollars, Canada has been suffering for some time now.

For those who noted my argument was a little weak, stay tuned. I plan on fleshing it out more thoroughly in the weeks to come. This isn't a week-long trade.

Chart of the Week

I am leaving you with one of my favourite charts. It's controversial. And all the financial theoreticians will tell you that there is no way the Fed's liquidity affects stock market returns on a day-to-day basis. Well, I don't believe them. And I don't think that my pal Barton_Options does either because he has made this chart of the S&P 500.

Look closely at the inlaid chart with the blue bars and yellow points. The yellow points represent the combined liquidity of the Fed's liquidity combined with the changes in the TGA (Treasury General Account). It's obvious there is a rough relationship there. If you would like to hear Barton explain it all, take a listen to the podcast I do weekly with Patrick Ceresna called Market Huddle. For Barton's episode - click here.

Thank you for reading and

have a great rest of the weekend,

Kevin Muir

the MacroTourist