Weekend Colour Commentary

The MacroTourist's best finds of the week

I'm trying something new for my last post of the week. Often I get a ton of great feedback to my articles. It seems a shame to not share the insightful comments (that are often better than anything I wrote) with the rest of you. Therefore, I have decided to make a weekly wrap-up post which highlights some things that I believe deserve your attention. Some of it will be comments directed to me, other stuff will be items I have found through other sources.

So let's jump to it!

This Week's Must Follow

Let's start with my week's recommendation of a strategist who I think everyone should have at the top of their twitter feed - Jim Bianco.

Apart from having the nicest looking charts in the biz, Jim offers a unique market perspective that often makes me think (and then say to myself, "why didn't I come up with that?").

To get a sample of his work, I am including a link that he has as his pinned tweet. It's a handout from his presentation from the Inside Fixed Income ETF Conference in San Diego. Click here to download the presentation.

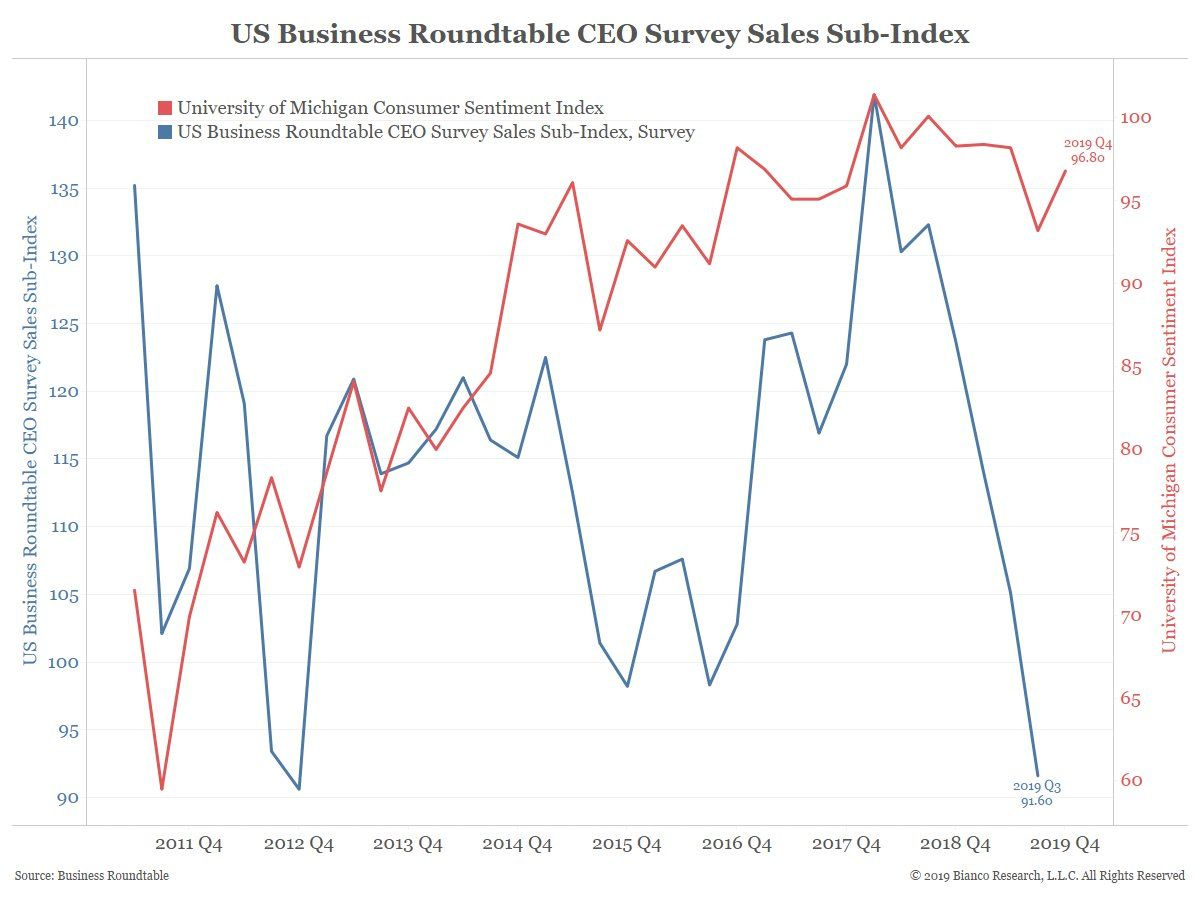

And here is a great example of the detailed economic data from Jim's shop:

Michigan consumer confidence was also out this morning and it upticked again to 96.8. I think this is a reflection of the new highs in stocks. But CEO confidence is going the other way. Again, no consistency among the survey data.

Best Podcast of the Week

When people ask me what podcast they should listen to, the first one out of my mouth is often Ted Seides' Capital Allocators Podcast.

I can't tell you how much it has made me a better investor. When it comes to serious money management, the quality of Ted's guests are second-to-none. And Ted does a bang-on job as an interviewer - really getting to the heart of the matter in a fun and entertaining way.

For me, last week's interview with Dawn Fitzpatrick of Soros Fund Management was a particularly engaging and educational episode.

Click here to be taken to Dawn's interview.

Feedback on MacroTourist Posts

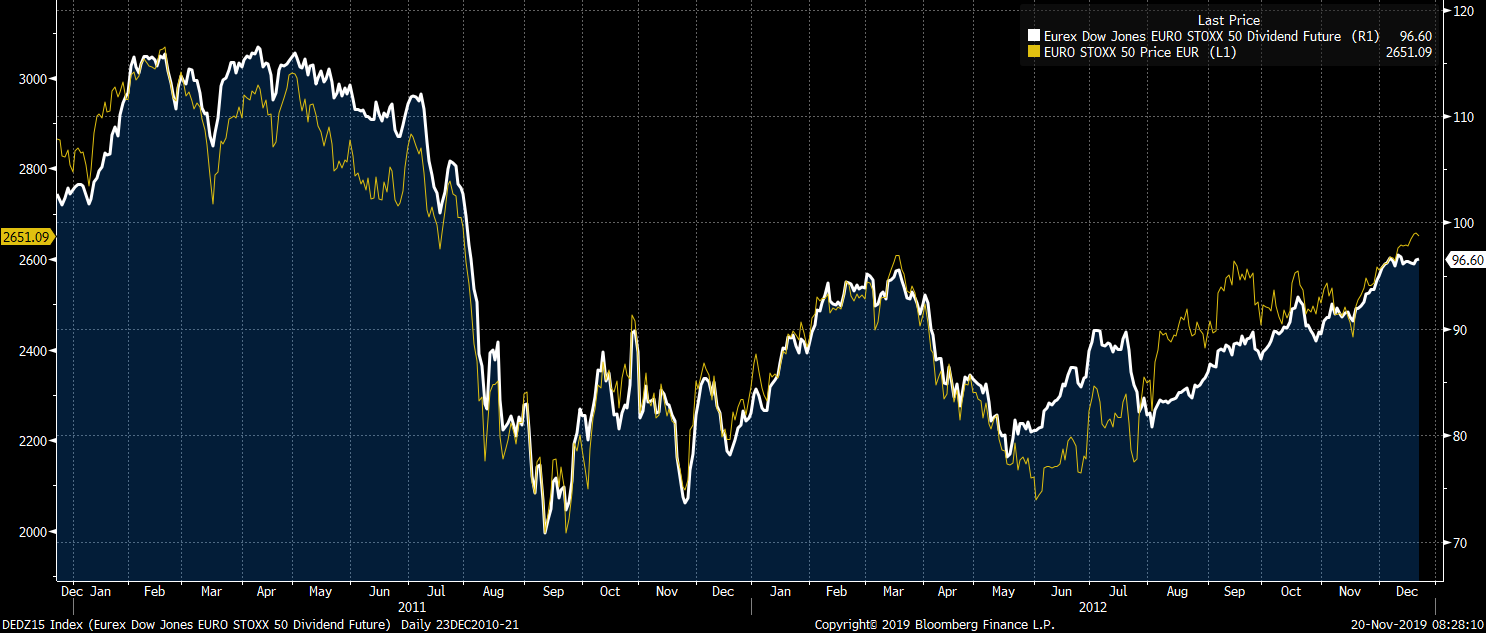

It was fun to write about the side-effects of the increasing popularity of Equity Linked Notes. I enjoyed hearing from my European friends who agreed with my analysis of the potential profit opportunities from the perpetually cheap forward Eurostoxx dividend futures. Here was a typical response:

We’ve been trading the SX5E dividends for many years, it is truly the gift that keeps on giving. Only caveat is make sure to always trade the long-end (to avoid surprises on the short maturities) and keep rolling.

However, there were some who were not quite as optimistic:

(we have some guys on the desk that traded this a few years ago. They refer to it as a widow-maker and it's much less attractive than it used to be, so they just ignore it now)

This same trader shared a terrific article titled The Great European Dividends Caper by Byrne Hobart. If you are interested in this trade, take the time to read this. It's well done and digs deeper than my post.

As for the specifics of hedging Equity Linked Notes, my article triggered an email from an old colleague about the delta sensitivity as it relates to the long-term dividend assumptions. Jeff Eichenberg used to sit across the desk from me at RBC Dominion Securities. In my mind, he is the guy who suggested I take my wife to Gotham Bar & Grill for her surprise 30th birthday, so I can't help but smile with good memories when he wrote to tell me:

I am very aware of this risk as I was the seller of all that stuff up there many years ago. It posed a very interesting dilemma. Do you price and trade/hedge long term equity options with a dividend yield or a discrete dividend flow? I believe the market does it with a yield but but how often do you change your yield assumption? When the markets were pretty volatile in the late 90’s and there was a decent dividend yield in Canada it was very meaningful. If you have $1 billion of options and are using a 2.00% yield and the market moves down 10% do you now use a 2.20% yield or do you stick with 2%? Good question. The answer is very important because it changes your delta and option price significantly on 5-7 year options. The big effect is really on delta. We ended up modeling a discrete flow 5-7 years out so we didn’t have to change our yield assumption for every move in the market. This is useful when dividends are lumpy but also kind of ridiculous at times because who know what stocks will even be in the index 5 years from now!

But the real comment that made me laugh was another buddy who said;

Enjoyed this, took me back to my deriv sales years.

You may know this, but there are also listed dividend swaps on NKY and HSCEI. NKY could potentially be bought with some confidence if you did the homework (and I haven't had a look at all) because there are proper accounting standards and some form of corporate governance in Japan. HSCEI is heavily influenced by the Beijing government and I don't trust the financial reports, so company fundamentals don't have the same importance.

He then reminded me that a famous hedge fund was long gobs of European dividend futures going into the 2008 Great Financial Crisis and ended up getting crushed on the trade.

The reason I share this story, is just to remind you that even though divs seem very cheap today in a benign environment, if we have a crisis, these things will go from cheap to way cheaper. Also there are no natural buyers of divs, just hedge funds and traders who are speculating.

Yeah, I hear that last comment loud and clear. In a bad market, this trade has the potential to get even more stupid cheap.

And I'll leave you with one last thought from the MacroGoose:

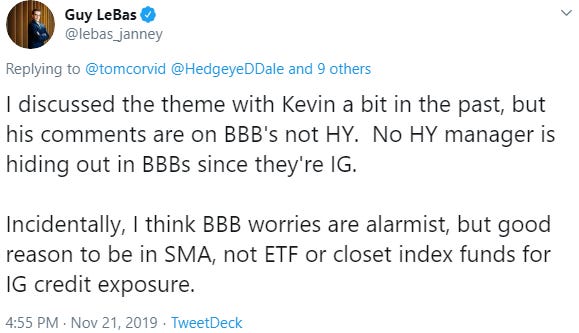

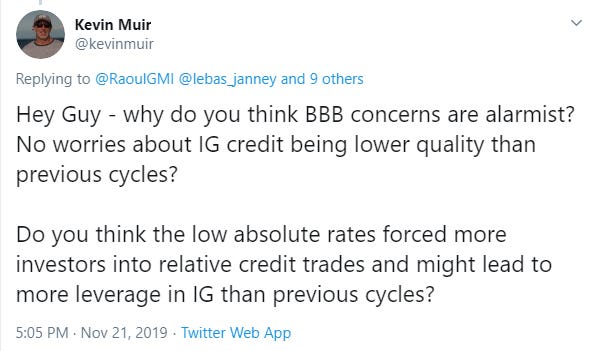

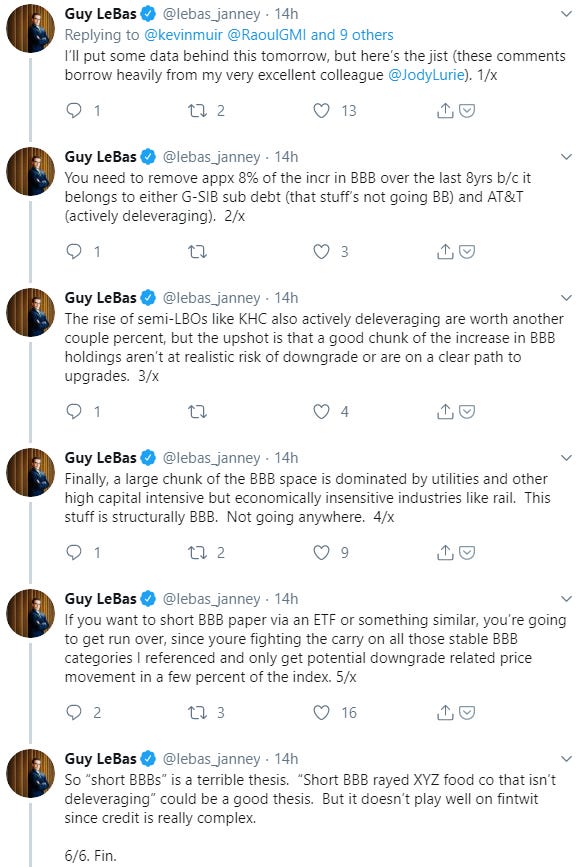

My article about the all-time-record-bulge of BBB's within the Investment Grade universe generated a ton of feedback.

I like to hear when others disagree with me - it keeps me honest - and no one seems to enjoy that task more than Janney's Chief Fixed Income Strategist - Guy LeBas.

And as usual, Guy jumped right into it:

Some great arguments there from a strategist who knows the technical in's- and-out's of the Investment Grade Index.

However, for those who want to see a good discussion devolve into a twitter battle between some pretty big fintwit heavyweights, take a gander at the whole feed. It often branches out and there was definitely some heated conversations. If you are interested, start at this link. Good luck! I never knew BBB's could such an emotional topic.

On the other side of the coin (you know, someone who might actually agree with me), a reader was kind enough to highlight GMO's Peter Chiappinelli's presentation from this Fall's Grant Interest Rate Observer Conference. Unfortunately I cannot share it with you as it is a paid-for-product, but man-oh-man, it makes me upset that I didn't attend that event. It's probably one of the best presentations highlighting the risks to credit markets that I have seen in ages. It's not emotional. It's not hyperbolic. It calmly sketches out the poor risk reward that is BBB's investing at these levels.

If you have access to Grant's, then I suggest you hunt the presentation down. If not, here is a link to an old GMO public article from Peter. I know that this has made me put Peter's writing to the top of my pile, and also ensure I don't miss the next Grant's conference!

Although I understand the argument that BBB-risk might be overstated, all this debating has not changed my mind. I am going with Peter on this one, and sticking to my belief that this risk is a time-bomb in the making.

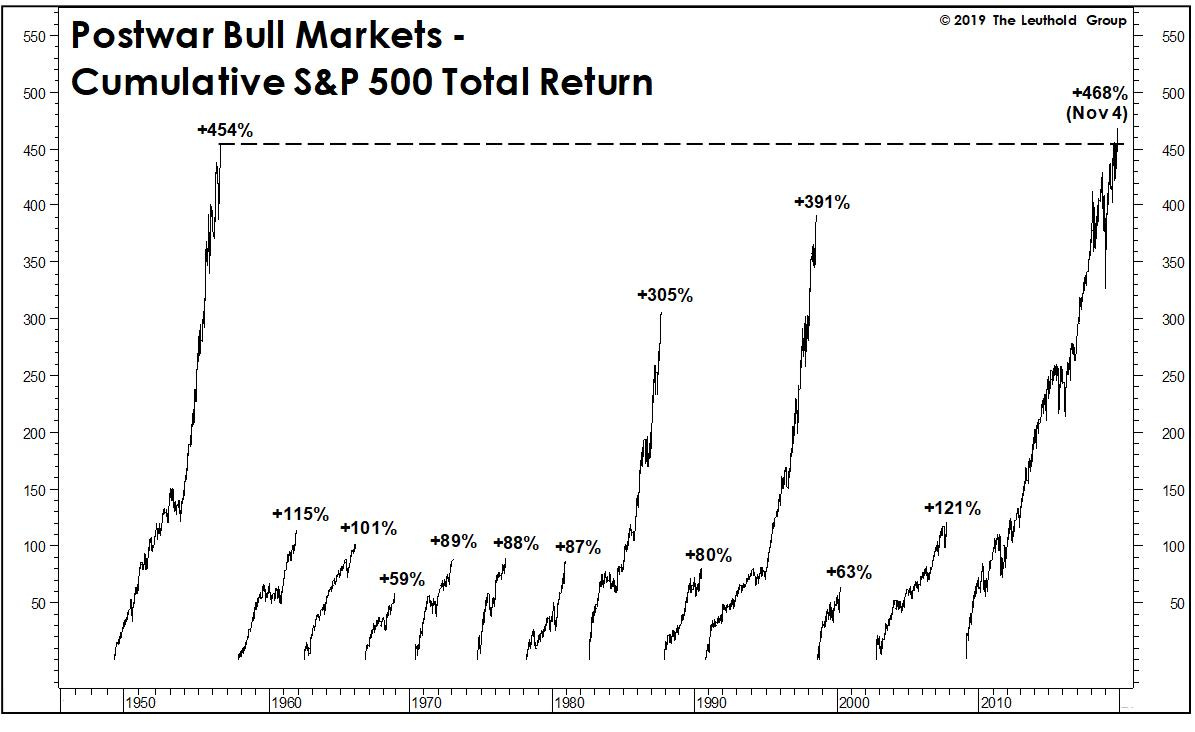

Chart of the Week

Last thing I will leave you with is my favourite chart for the week.

Thanks for reading,

Have a great rest of the weekend,

Kevin Muir

the MacroTourist