TRYING TO SAVE THE ECONOMY WITH LOWER OIL

The other day President Trump tweeted the following:

Contrary to some of his tweets, this one seems to make sense. After all, the price of energy goes into everything. From the cost of manufacturing household items to shipping foreign foreign-made goods from overseas to the price filling up the tank on the commute to work, it’s tough to argue that reducing the price of energy isn’t a huge wealth boost for the average consumer.

Surely this must be easy to observe in the economic data. A decrease in the price of energy must mean a bump in economic activity.

Well, unfortunately for the President, there is a relationship between energy prices and economic growth, and it is indeed negatively correlated, but the lag is long. Much too long for a President that measures his performance by the daily newscycle.

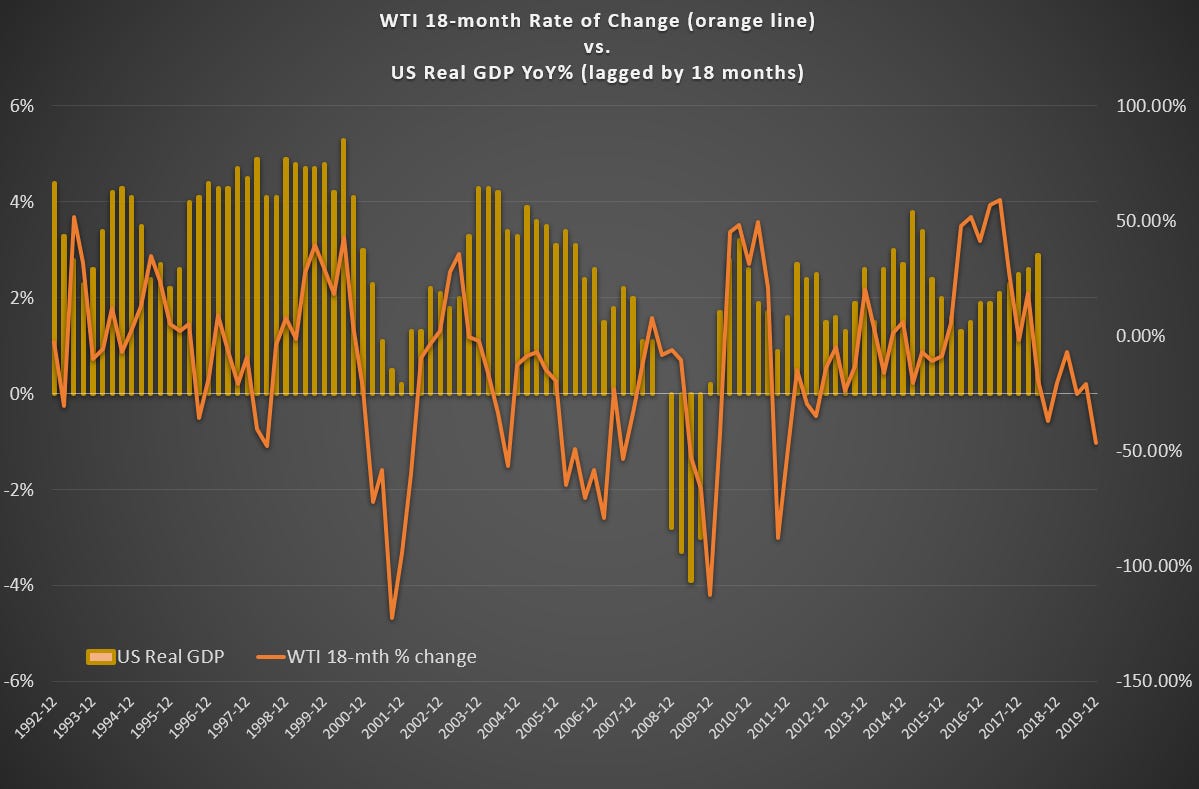

Let’s look at the data. Here is the chart of US Real GDP growth (lagged by 18-months) versus the inverted 18-month rate of change of WTI Spot.

So what’s this showing? The orange line is the inverse 18-month rate of change for WTI. So when it is going down, that means the price of WTI has been rallying for the past year-and-a-half. Look at the relationship between that change and the economy. Sure, there is a definite correlation, but the lag is… how would President Trump say it? Yuuuggggeeeee.

If this relationship continues, we should expect another 18 months of economic weakness before the benefits of the lower energy price kick in.

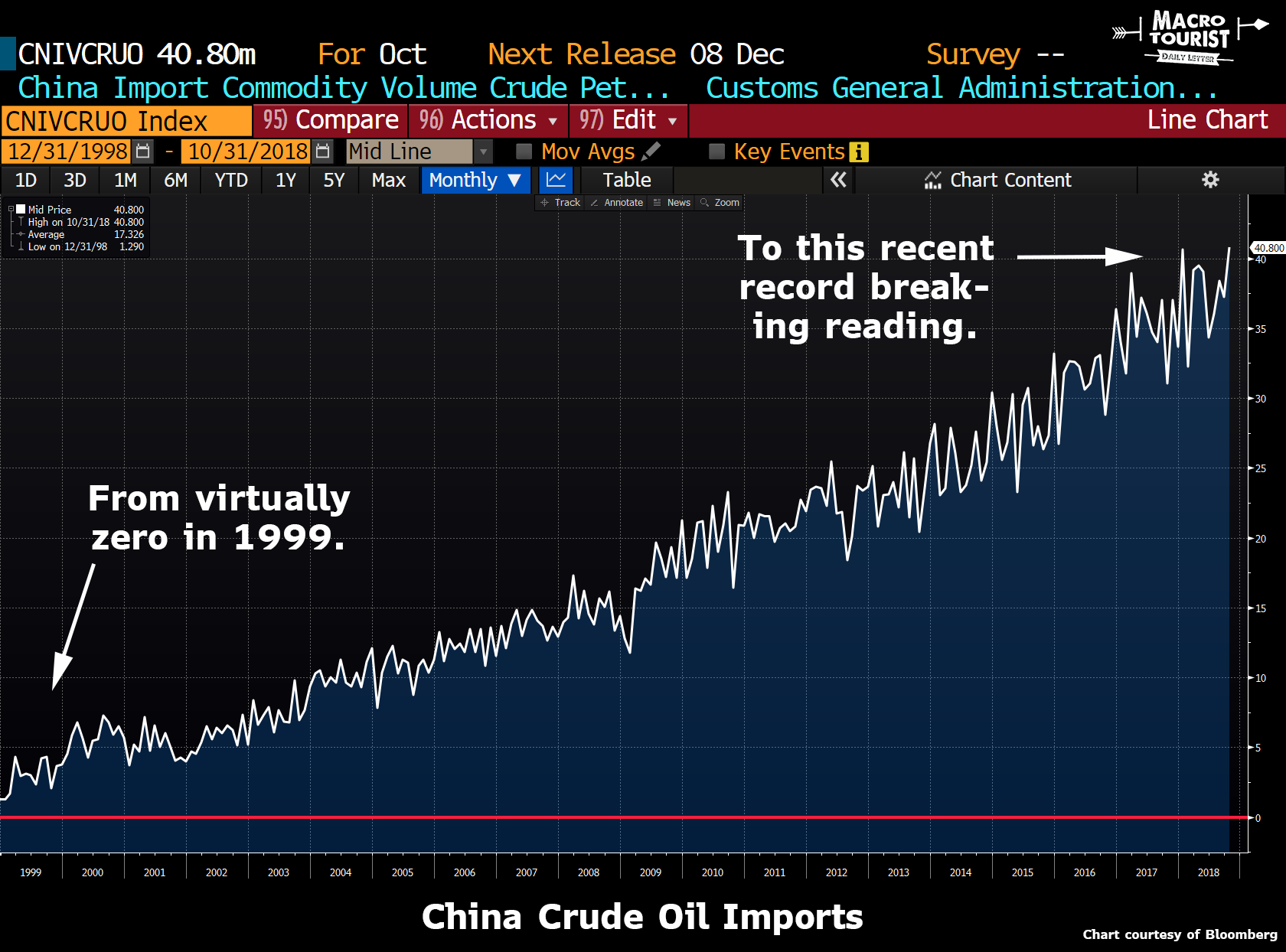

And far be it from me to question the President’s tactical decisions, but Trump seems intent on applying as much pressure as possible on China to extract a more fair trade deal. Last I checked, China was the largest importer of crude oil in the world.

I can almost hear the Chinese trader in the NYMEX pit come running out from his booth during the recent oil price decline with palms facing inwards screaming “BOUGHT FROM YOU!!!”

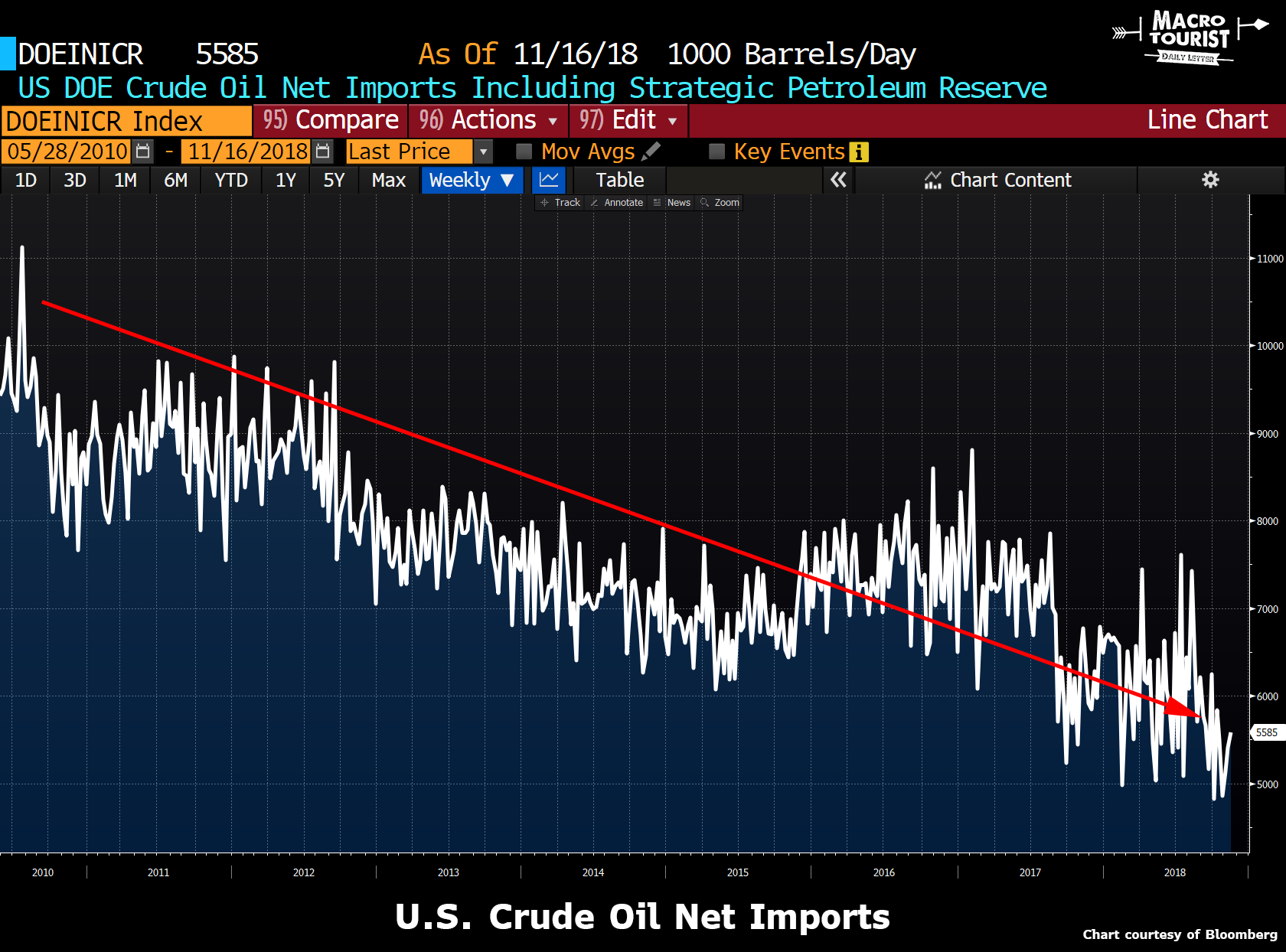

In the meantime, the U.S. has almost halved their net imports during the past decade.

The true extent of the benefits of the decline in the price of crude oil is difficult to judge, but here is another aspect where I happen to agree with the President. If the Fed doesn’t monetize the decline through marginally lower rates (it doesn’t have to be actually lower rates, but it does need be lower than would have otherwise been the case), then the decline in crude oil might not be as much a benefit as many of the economic bulls believe.

Now don’t misconstrue my remarks. Lower energy prices are a net benefit to the entire global economy. It’s just that it probably isn’t as immediately beneficial to America as the President wants…

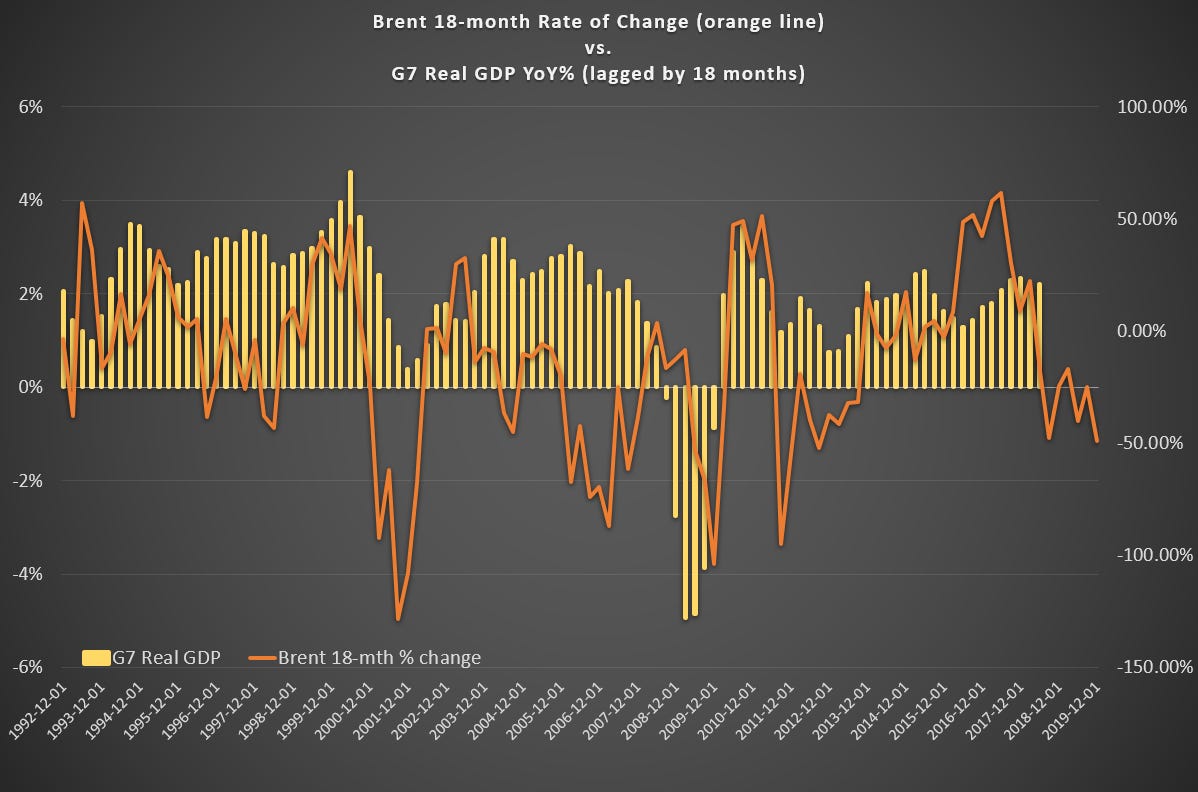

I will leave you with one last chart. This one is Brent lagged versus G7 growth.

It certainly appears like the next ticks in the global economy are lower, not higher.

Thanks for reading,

Kevin Muir

the MacroTourist