THE OTHER VANNA

Watch for changes in volatility moving the underlying market

Do you ever hear the "cool kids" in the option world talking about "vanna" and wonder what they are referring to? They seem obsessed with Vanna's moves. Thinking it was strange they were so interested in a game show host, I did a little research.

My conclusion? If you ever hear anyone making jokes at Wheel of Fortune's Vanna White's expense, they are idiots. This woman has got it all figured out. She works four days a month, makes somewhere between $4 and $10 million a year, and is worth more than $100 large. Vanna is a genius!

It still seemed strange that Vanna was constantly been cited in option trading forums, so I kept digging. It took me a couple of months, but I eventually figured out that SPX option traders were not talking about Vanna White. Instead they were talking about another convoluted mathematical option concept.

Vanna is the change in delta due to a change in volatility. Got that? Yeah, I know, these option traders love giving fancy names for complicated second derivative-type measurements.

However, instead of just blowing this off as the domain of finance geeks, I suggest you take the time to understand this concept as it is driving market moves much more than you probably guess.

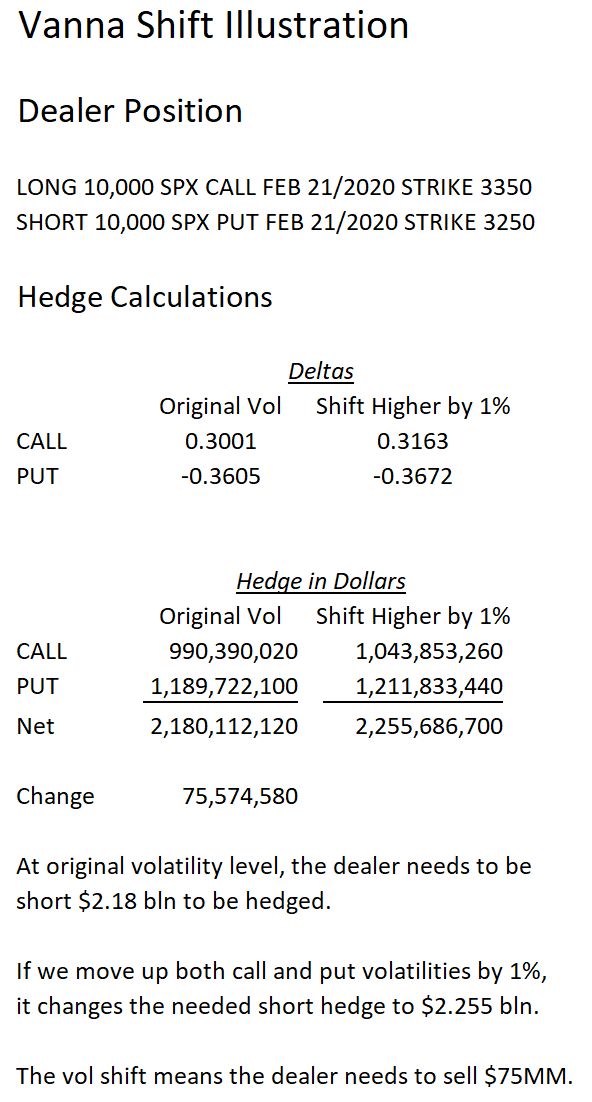

Probably the easiest way to explain the concept of vanna is to make an example. Once again I will create a typical dealer position. Please note I am aware this is a huge generalization and if the dealers' position are different, then vanna could be the exact opposite of my analysis. However, this is how dealers have been typically set up over the recent past.

For my example, I am altering the hedging volatility of both the call and put higher by 1%. The call was originally 11% and it moves to 12%. The put was 16.5% and it rises to 17.5%. In the real world, the put probably rises more than the call, but the purpose of this exercise is to show the change in delta as volatility rises, so I thought I would just keep it uniform.

What's important to note is that the simple act of shifting volatility higher results in dealers having to increase their short hedges.

Take a moment to think about the ramifications of vanna. For example, if Trump came out tomorrow and said, "if elected, I will lower corporate tax rates by another 500 basis points." And let's say Bernie was the Democrat's candidate. He then responds with, "if elected, I will raise corporate tax rates by 500 basis points." Now, let's assume a dead-heat between the two candidates. Most people would contend there should be zero change in the level of the stock market with this development. After all, both outcomes are equally likely. However, I would suggest the market should be lower in such a scenario. Dealers would be forced to increase the volatility of their book as the projected move either way would be larger. This would result in vanna selling to hedge their positions.

In real life, dealers usually mark their books' volatility higher from an event that causes a sudden increase in price movement. This morning's Chinese flu is a perfect example. With the gap lower, volatility has increased. As dealers increase their volatility assumptions to reflect this new reality, they have to sell more deltas. This can sometimes feed on itself with their selling causing underlying prices to fall, which then causes volatility to rise which causes even more selling.

On the flip side, quiet markets that grind higher can cause volatility to be lowered resulting in the dealers having to buy deltas.

Some people claim VIX reflects the volatility of the underlying rather than leading it. However, as the option market's size and the popularity of other volatility strategies has increased, it is becoming more of a self-reinforcing process with changes in VIX causing changes in the underlying asset.

Vanna White knows enough to watch for dealers' adjustments potentially causing large moves in the underlying, so should you.

Thanks for reading,

Kevin Muir

the MacroTourist