Market is assuming Fed reaction function hasn’t changed

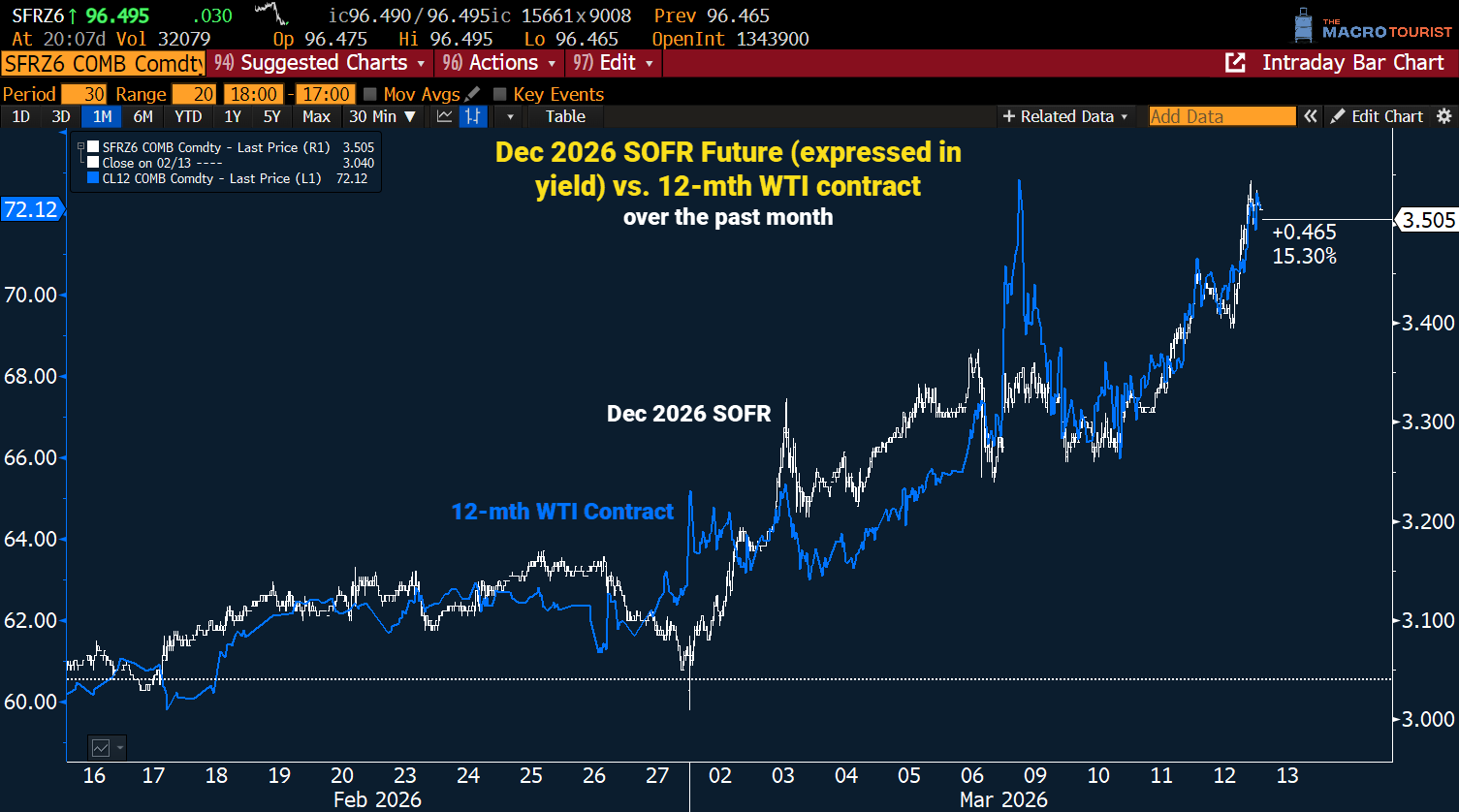

As the price of crude oil has risen, the front-end of the yield curve has backed up (rate has risen). For example, the Dec 2026 SOFR contract had a forward yield of 3.15% priced in before the Iran/US/Israel war started. In the initial days of the war, the forward rate declined to 3.05%. However, as the price of crude rose, so did the forward yield.

This is the price of the 12th-forward WTI futures contract vs. the Dec 2026 SOFR Future (expressed as yield).

The forward rate has risen almost 50 bps over the last two weeks! The market has taken out two cuts because of rising crude oil.

What I find most fascinating about this market action is that there has been little change in the market’s expectation about the Fed’s reaction function.

For all the talk about Kevin Warsh running the economy hot, right now, the market is assuming that the FOMC will continue a somewhat traditional response to higher inflation due to an energy spike.

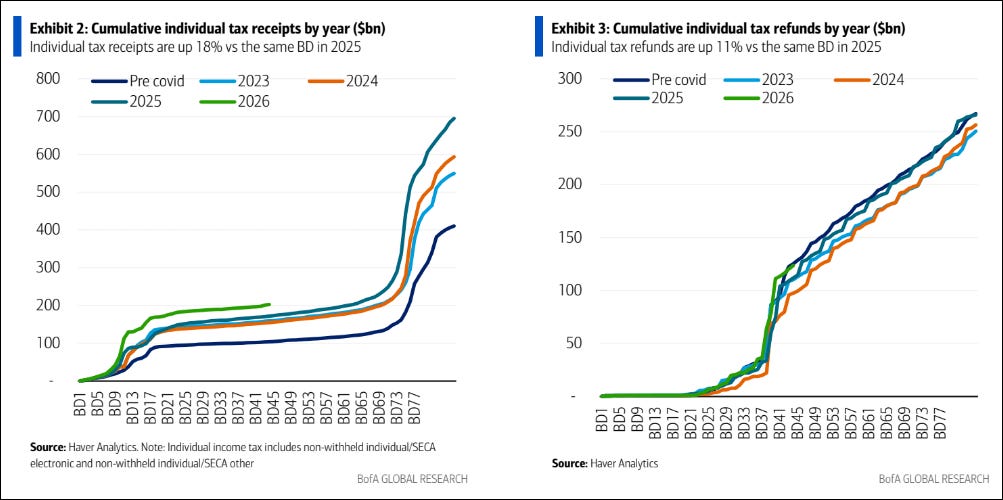

Tax receipts versus refunds

There has been a lot of debate about the underlying strength of the economy. The bulls look at the tax receipts and say, “they are running above normal so the economy must be doing better than market realizes.” The bears look at the tax refunds and lament, “everyone is counting on this big stimulus from refunds, but it’s just not in the data.” Pick your fighter, but BofA has a chart that shows both side by side.

(personally, I think tax receipts are higher because of stock market cap gains, but we will see…)

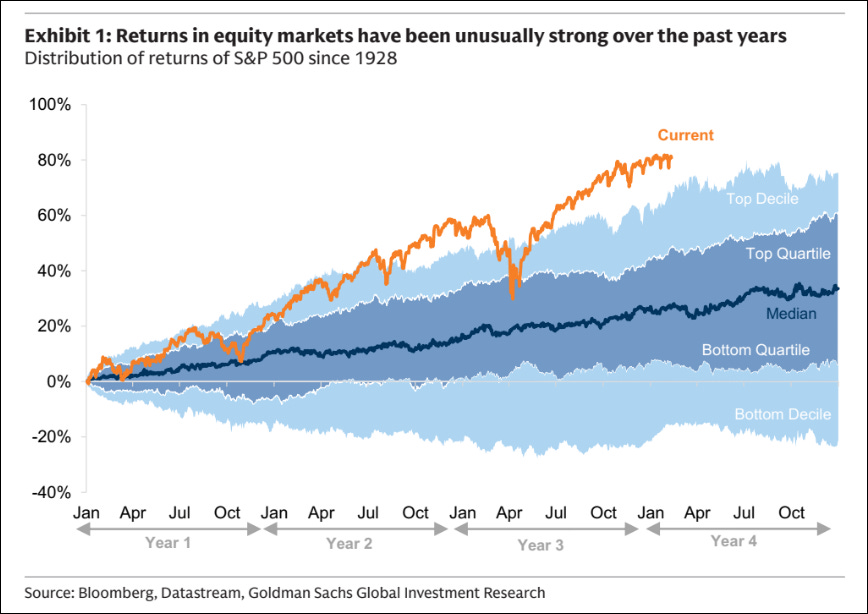

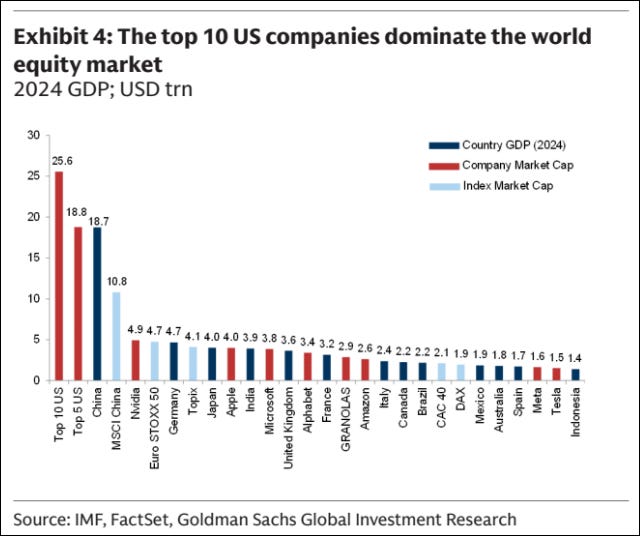

Goldman stock market charts:

This bull market is unusually strong.

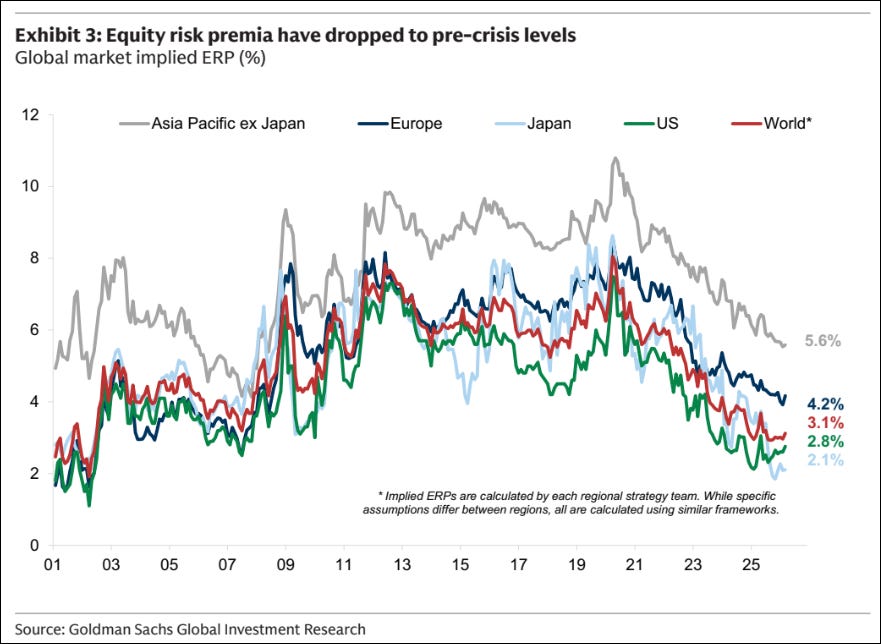

And as would be expected in such a strong market, the equity risk premium has collapsed.

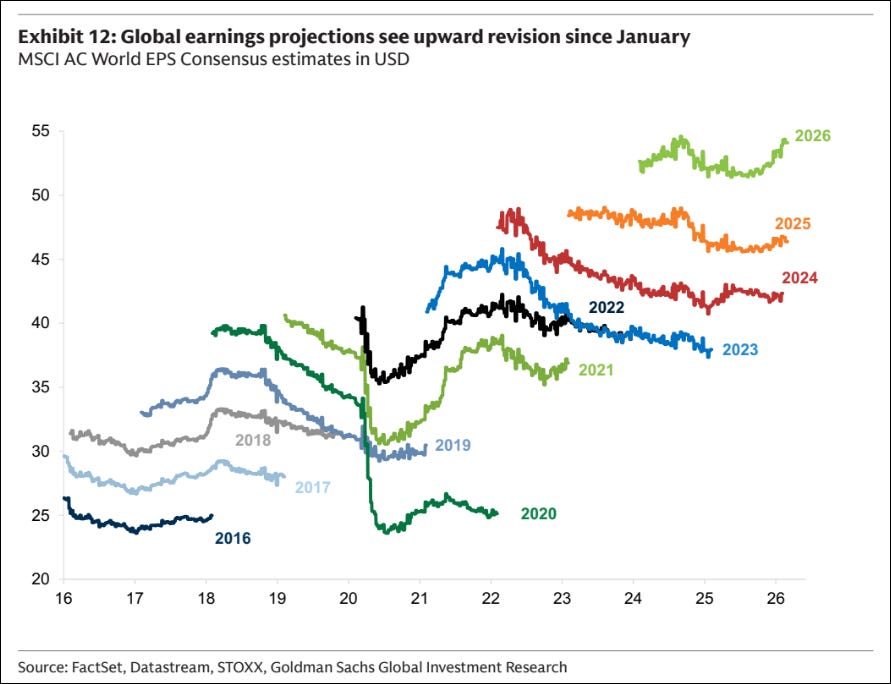

I found this chart of global earnings interesting. Maybe the economy really is strong. Usually at this stage of the cycle, front-year EPS forecasts would be declining. Instead, they are rising.

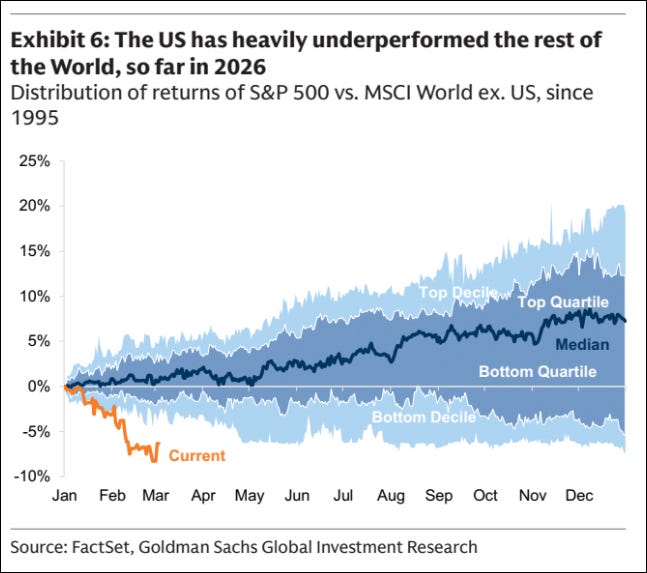

But before you get too excited about US stocks, here’s a chart that surprised me. I knew 2025 was bad, but I didn’t expect the US to be unperforming in 2026 so badly.

And don’t ever forget how much room there is for them to correct.

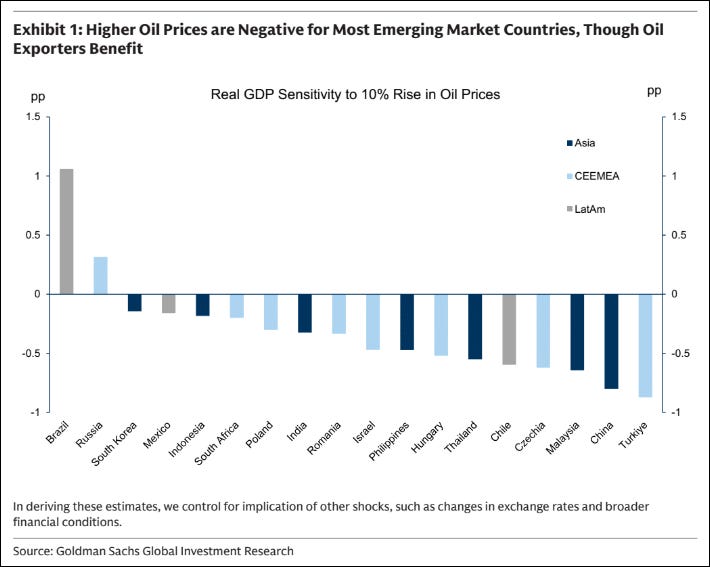

The emerging market currency to own

One last chart from Goldman… If there was ever a time to own Brazil over the other EMs, maybe this is it?

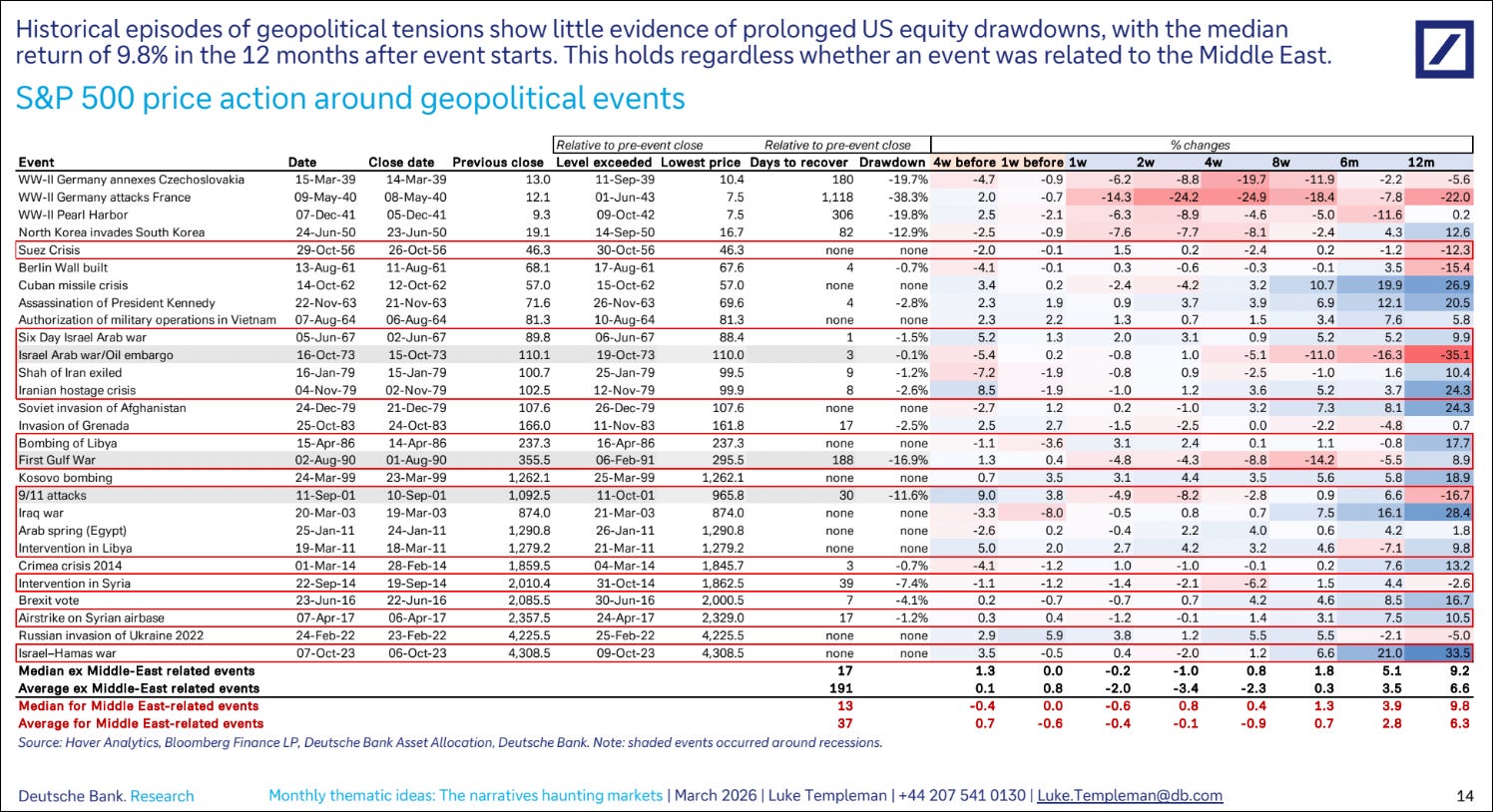

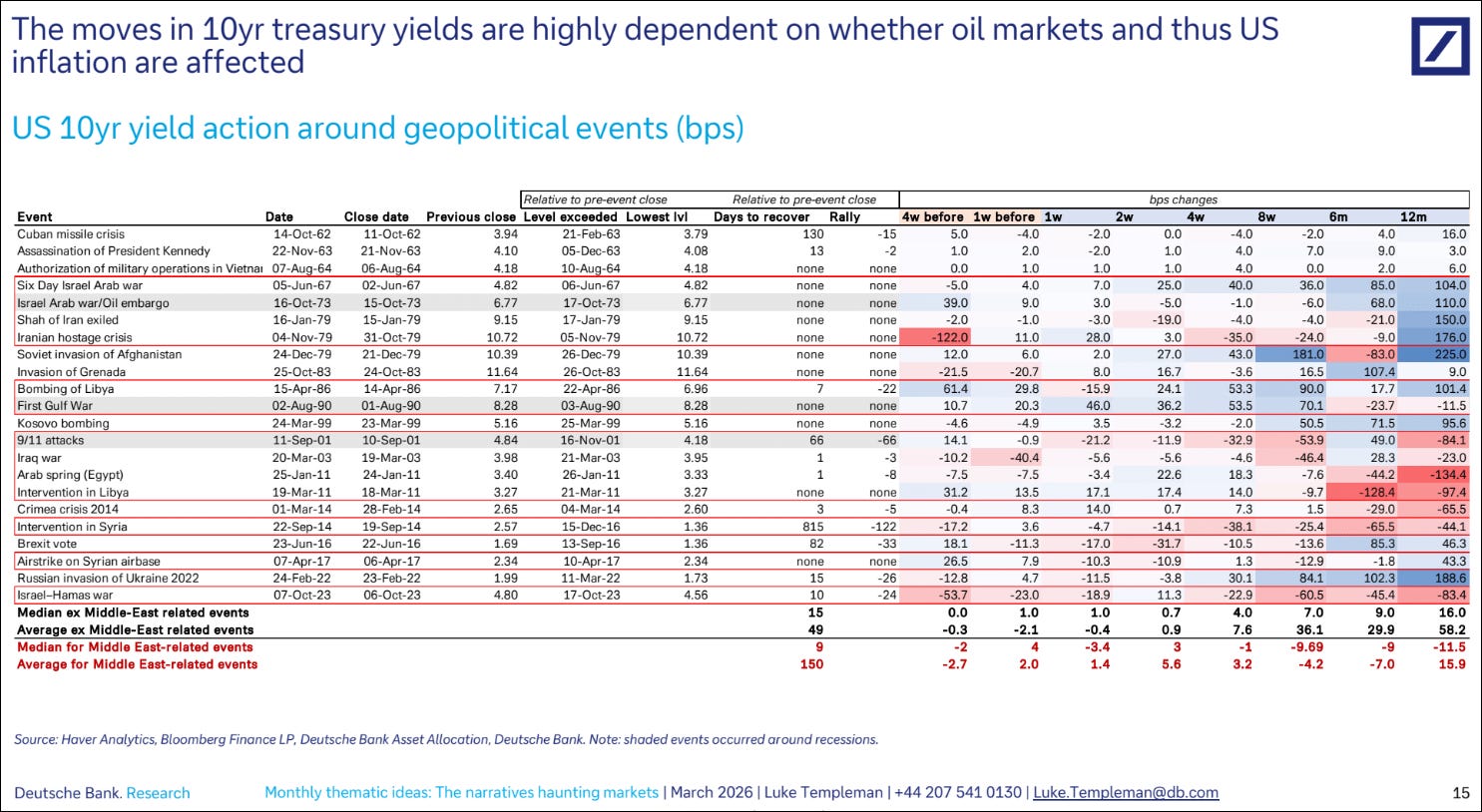

Today in “geopolitics never matters”

I have tongue-in-cheek highlighted all the “buy the dip” calls regarding the Iran/US/Israel war. Today’s installment comes from DB:

Hey Kev. Thanks , this is great stuff ! I bought EWZ last quarter and slowly adding but the perspective of energy independence is something that wasn’t on anyone’s radar before the war broke out. I’m wondering if there will be a permanent risk premium on oil? And if net oil exporting EM countries can benefit ?

https://x.com/ojblanchard1/status/2032053039566070081?s=46&t=o0ltzjzQJtNKHKg0l0lx6A

This is what the Professor Emeritus of Economics at MIT had to say this morning. It reminded me of your interview with Marko. I think he said something along the lines of “ Trump will taco but the Iranians will not eat the taco “.

I guess it takes 2 to taco.

Thanks again