MNUCHIN MASSIVE CHRISTMAS EVE BOTTOM?

Can’t deny that it’s been a wild few weeks in the financial markets. Although it seems like an eternity, it’s only been ten trading days since U.S. Secretary of the Treasury, Steve Mnuchin, called a special meeting of the President’s Working Group on Financial Markets to ensure that banks had “ample liquidity”. It was Sunday night, a day before Christmas Eve, and the stock market had been falling precipitously for the previous few weeks. Mnuchin was under a lot of pressure from Trump to fix the problem and he figured he needed to do something.

So Mncuchin interrupted his Cabo San Lucas vacation to calm markets. After all, nothing exudes confidence more than making a few phone calls from your Mexican resort to the top six bank CEOs to confirm they don’t have a problem with liquidity. Especially when absolutely no one was ever claiming liquidity was an issue.

Now many blame Mnuchin’s brain-dead move for the massive sell-off on Christmas Eve. After all, the day before Christmas is usually a slow trading day with markets closing at 1pm as traders rush off to do their last-minute shopping.

Yet instead of a slow listless trading day, it was an absolute bloodbath reminiscent of a Game of Thrones episode. The S&P 500 future closed down 71 handles - almost 3%!

Was it Mnuchin’s fault? Who knows? I don’t think he helped.

But what many overlook is that stock market futures were initially up on his stunt. Sunday night after his announcement, spooz were trading up more than 20 points.

Granted, by the time the cash market opened at 930am the stock market had given up those gains, but if we look at the intraday chart, after an initial dip right after the open, the market looked like it might bottom. By 1030am we were approaching unchanged on the day, and then it happened.

There was a monster wave of selling that took the S&P 500 down a sickening 3% in the last three hours of trading. It was illiquid and made little sense for traders to demand liquidity on the day before Christmas, yet they were spooked and took a “shoot first ask questions later” attitude.

And what drove this panic?

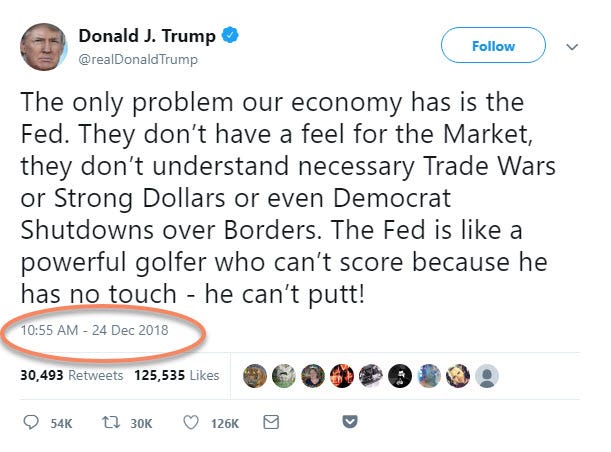

Look at the timestamp on Donald Trump’s twitter post:

I don’t want to bother discussing whether Trump is correct in his assessment of the Federal Reserve’s policies. Who cares? It is what it is. I don’t want to end up one of those old men yelling at clouds.

I am only interested in what it means for the market, and it is my firm opinion that Trump’s ongoing feud with the Federal Reserve contributed to a collapse in confidence that caused the financial market sell-off of December.

Fed watchers anonymous

I was out for dinner with a good buddy last night and he remarked that I had become one of those Fed watchers that I used to make fun of. You know the type - desperately trying to explain every tick through slight nuanced changes in Fed officials’ language.

Yet my response was that the Fed was all that mattered lately. I would be foolish to ignore the 10%+ swings due to the comments from both the Federal Reserve and the President.

And I contend that predicting Powell’s moves in the upcoming quarters will mean more than trying to come up with a fundamental fair value for financial assets.

I will quote my favourite macro trader Stanley Druckenmiller when it comes to what moves stock markets (a Macro Ops post that’s actually from a 1988 Barron’s interview)

The major thing we look at is liquidity, meaning as a combination of an economic overview. Contrary to what a lot of the financial press has stated, looking at the great bull markets of this century, the best environment for stocks is a very dull, slow economy that the Federal Reserve is trying to get going. Once an economy reaches a certain level of acceleration. the Fed is no longer with you. The Fed, instead of trying to get the economy moving, reverts to acting like the central bankers they are and starts worrying about inflation and things getting too hot. So it tries to cool things off… shrinking liquidity… [While at the same time] The corporations start having to build inventory, which again takes money out of the financial assets… finally, if things get really heated, companies start engaging in capital spending… All three of these things, tend to shrink the overall money available for investing in stocks and stock prices go down.

Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.

Although I would love to ignore Jay Powell and his flip-flopping remarks, the reality is that after Trump’s “Fed has no touch and can’t putt” comment, Powell caved and caused the following rally:

So yeah, I have become a Fed-watcher as the market is trading more based on Powell’s comments than any sort of fundamental metric.

Stepping back

What changed that made the Federal Reserve so important? After all, Jay Powell has been the FOMC chair since November 2017 and you could argue that policy has not been altered.

Under Powell’s tenure, the Federal Reserve has consistently raised rates and wound down the balance sheet. Powell has been steadfast in his execution of this tightening campaign.

Yet even the most ardent hard-money advocates will admit that eventually, money will be too tight. At some point the Federal Reserve will have tightened too far.

Here is where the heart of the problem lies. What is that level? And to determine that level, should the Federal Reserve take into account market-based-signals or should they focus more on traditional economic indicators?

And to make matters even more complicated, is the Federal Reserve truly worried about inflation, or are they more concerned about a growing financial asset bubble?

Getting into Jay Powell and the rest of the FOMC Board’s heads to understand their reaction function as the economy evolves will be paramount to forecasting financial asset returns in the coming quarters and years.

So without further ado, here is my interpretation of what Powell is trying to accomplish and what that means for the markets.

Although the Federal Reserve mouths words about being concerned about inflation, the reality is that they have been consistently undershooting their target, and it’s been over a decade since Core PCE inflation has been above 2%.

Is the Federal Reserve worried about inflation? Do they really think that’s the biggest risk out there?

I call bullshit on that one. Don’t forget that Bernanke is “100% confident that he can control inflation”. I know Powell is a different kind of Fed chair, but the confidence within the Federal Reserve runs deep in regard to their ability to quash inflation if it rears its ugly head.

We haven’t had a real inflation problem in decades. The idea that Powell lies up at night worrying about inflation is laughable.

But I think Powell has a demon that haunts him. Jay was nominated to the FOMC Board by President Obama in December 2011. Since then, he has repeatedly cautioned about quantitative easing and other extraordinary monetary stimulus measures.

I believe Powell understands all too well the massive cost of the Great Financial Crisis in both economic and human terms, and his biggest worry is not inflation taking off, but instead the expansion of a massive financial asset bubble that, when eventually pricked, will have even greater repercussions.

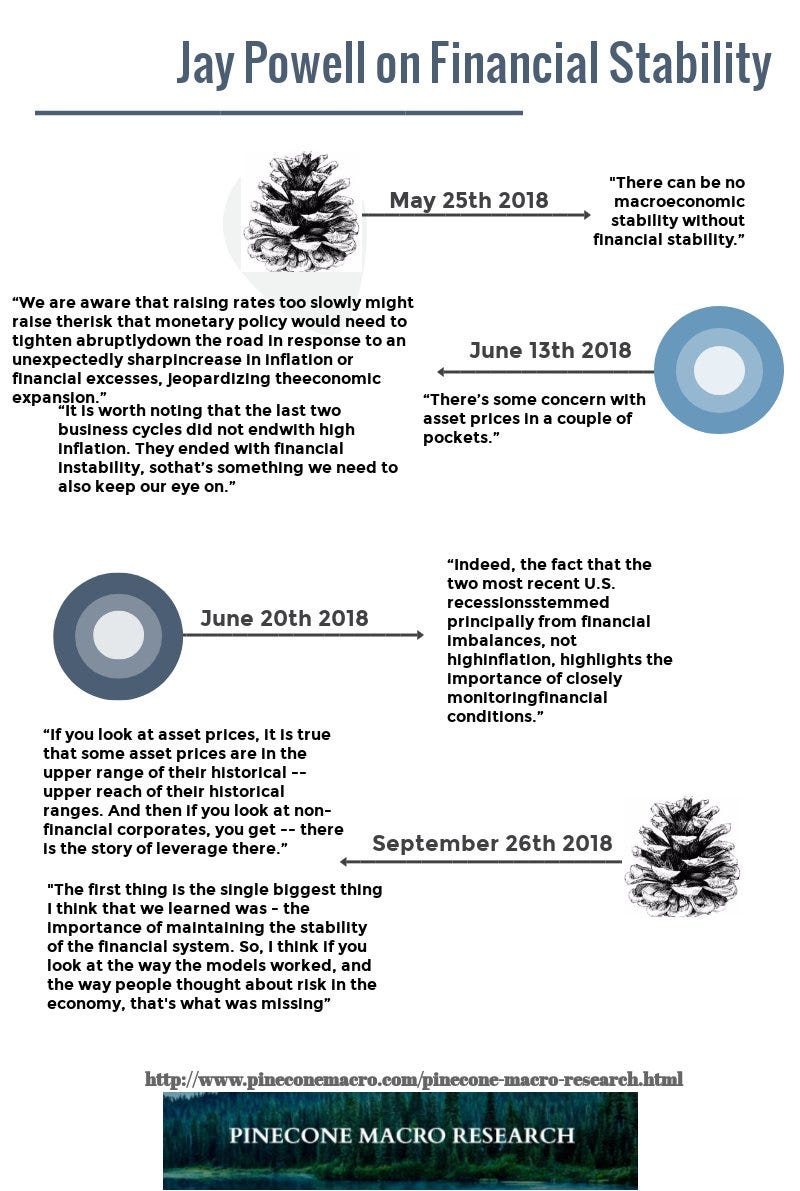

My friend Chase Taylor at Pinecone Macro did some great analysis digging up Powell’s quotes over the past year which highlight this reality (give Chase a follow on twitter, or better yet - check out his website):

My favourite quote? “It is worth noting that the last two business cycles did not end with high inflation. They ended with financial instability…”

Powell is not worried about inflation anymore than Bernanke was worried about inflation.

Yet he is much different than Easy-Ben.

Whereas Bernanke was concerned about using monetary stimulus to encourage wealth-affect spending, Powell views these distortions as ultimately counterproductive.

So Ben wanted to provide a floor for financial assets - you know, the infamous Fed put, I think Powell is more interested in selling a call. He wants there to be a ceiling so that another bubble isn’t created that ultimately pops and causes more economic pain.

Trump has been haranguing the Fed for quite some time, yet until recently, Powell has been impervious to the comments. Many strategists have shouted about inflation not being a problem and wondered why the Fed seemed so intent on raising rates. Yet in a private moment, I am sure Powell would agree with them. He isn’t worried about inflation. But the possibility of another massive financial bubble scares the shit out of him.

When you think about his recent actions through this lens, it makes so much more sense.

Why did he make the October 3rd comment that rates “were a long way from neutral?” Have a look at this chart of the S&P 500 and CSI BarCap high-yield spread going into that day:

Financial conditions were loose and showing absolutely zero signs of being sensitive to his tightenings. Powell was probably rightfully scared that the bubble would take off. Therefore he leaned more hawkish than he probably should have if he was simply setting rates purely from economic indicators.

But then what happened? From there, the market decided that Powell had just tightened into a recession and quickly priced it all in within the space of a month.

Plus it was made worse by Trump nattering about rising rates. It made Powell’s job of acknowledging the market signals all the more difficult.

So it appeared the Fed was tone deaf and intent on raising rate regardless of what happened to the financial markets.

It all fed onto itself in a crazy self-reinforcing cycle culminating in the infamous Christmas Eve sell-off.

Going forward

I will not make any judgment about what Powell should do, but will assert that Friday’s statement where he caved to the market forces was unproductive. Assuming that I am correct about his biggest worry being market bubbles, he has now set himself back. Stocks are screaming higher. Investors are once again chasing high-yield and other risky forms of debt.

It won’t be long until he will be forced back into trying to talk the markets back down.

Inflation isn’t his worry - market bubbles are his over-riding concern.

Remember back a half-dozen years ago when all the hedgies were bearish and David Tepper came out and said something to the effect of; “if the economy weakens, then the Fed will ease and stocks go up. If the economy strengthens, then stocks will go up because earnings will be rising. Therefore I am buying.”

Well, I think it’s almost the exact opposite situation today. If the economy strengthens then Powell will hike and stocks will fall from the liquidity withdrawal. If the economy weakens, then Powell has shown he is loathe to come to the market’s rescue and he will be slow to lower rates.

I don’t think you need to overthink this. The Fed has tightened into either a slowdown, or a recession. The market sniffed it out, but the Fed ignored the signals for a bit and made the sell-off worse. Now the market is in the process of correcting that overreaction by rallying.

But don’t forget that Powell has absolutely no stomach for frothy financial markets, so beware getting too excited about the Fed’s recent dovish talk. This is not Yellen or Bernanke’s Fed. Powell has a different set of beliefs, and although he has succumbed to market pressures for the moment, it won’t take much for the old tone-deaf Powell to return.

I will leave you with a quote from Stephen Roach writing In defense of Jerome Powell’s courageous Fed. Although I am sure Stephen would most likely be disappointed by Powell’s recent change-of-heart, I think Powell’s waffling is only for the moment, and that Roach’s analysis is ultimately where Powell wants to head in the long run:

Predictably, the current equity market rout has left many aghast that the Fed would dare continue its current normalisation campaign. That criticism is ill-founded.

It’s not that the Fed is simply replenishing its arsenal for the next downturn. The subtext of normalisation is that economic fundamentals, not market-friendly monetary policy, will finally determine asset values.

The Fed, it is to be hoped, is finally coming clean on the perils of asset-dependent growth and the long string of financial bubbles that has done great damage to the US economy over the past 20 years.

Just as Paul Volcker had the courage to tackle the Great Inflation, Jerome Powell may well be remembered for taking an equally courageous stand against the insidious perils of the Asset Economy. It is great to be a fan of the Fed again.

Thanks for reading,

Kevin Muir